Focus Bank needed a platform that could work the way they work, preserving their existing workflow for qualifying applicants and matching them to the right products.

A meaningful share of Focus Bank's new CD accounts are coming from shift workers and others who can't make it to a branch during business hours.

By layering integrated fraud verification with a structured, attentive implementation process, Focus Bank built something more defensible than what in-branch processes could offer.

Focus Bank has been serving communities in Southeast Missouri and Northeast Arkansas since 1931. Family-owned and operating across 9 locations, the bank has built its reputation on personal service. Customers reach a real person, staff know their community, and nearly a century later, neither of those things has changed.

What has changed is the competitive landscape. Focus Bank competes directly with national banks and fintechs for deposits. With roughly $880 million in assets and a goal to cross the billion-dollar mark, the bank needed to grow core deposits. Certificates of Deposit were the vehicle, and to do that at scale, they needed a digital account opening platform that could match their standards. In August 2025, they found it with Narmi.

Focus Bank had a healthy loan pipeline and a clear growth target: raise $50 million in new deposits within 12 months. The problem was on the funding side, and the bank had very little digital infrastructure to work with.

Their account opening capabilities had been dormant since parting ways with a previous provider. Customers who filled out a website form got a service ticket. A call center rep followed up when they could. It worked often enough, but it wasn't scalable and it wasn't fast. Customers who couldn't take a callback or who simply lost interest in the meantime were gone. An entire segment of potential depositors, people working non-traditional hours, people who wanted to open an account at 10pm from their phone, had no real path in.

The goal wasn't just to reactivate a digital channel. It was to build one worth having, one that could actually reach the customers a branch-only model couldn't.

Flexibility was the baseline requirement going into the search. Focus Bank wasn't willing to flatten their existing process to fit a vendor's template. They needed a platform that could preserve their own logic for vetting applicants and routing them to the right products. That requirement narrowed the field considerably.

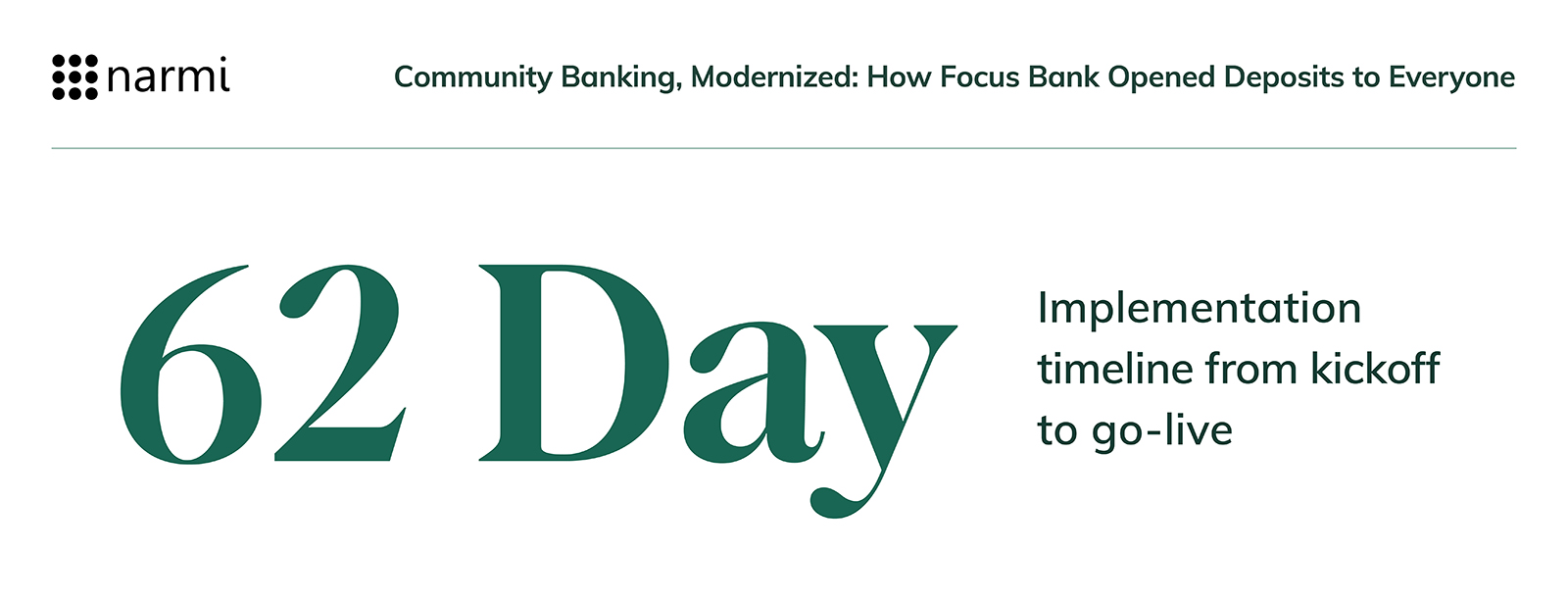

Once they found the right fit with Narmi, implementation moved quickly. Focus Bank went live 62 days after kickoff and the team worked through compliance requirements, fraud rules, and product workflows in detail. Staff-assisted functionality was built in from the start, so when an applicant stalls mid-process or an online lead needs follow-up, a team member can step in and continue the application directly rather than forcing the customer to start over.

The results showed up in unexpected places. Focus Bank's branches close before a 12-hour shift ends and open after one begins. Shift workers finishing at 7pm or starting at 7am had no window to get to a branch. Now they don't need one. That segment alone has been a meaningful source of early CD growth, and it's exactly the kind of customer the bank hopes to grow a full relationship with over time.

Reaching more applicants was the goal, but a broader pool also meant more exposure. The relationship-driven checks that worked at a teller window weren't built for the volume or risk profile of a digital channel. Focus Bank's BSA team also needed a verification process that was consistent and defensible during regulatory exams, and patchwork verification wasn't going to get them there.

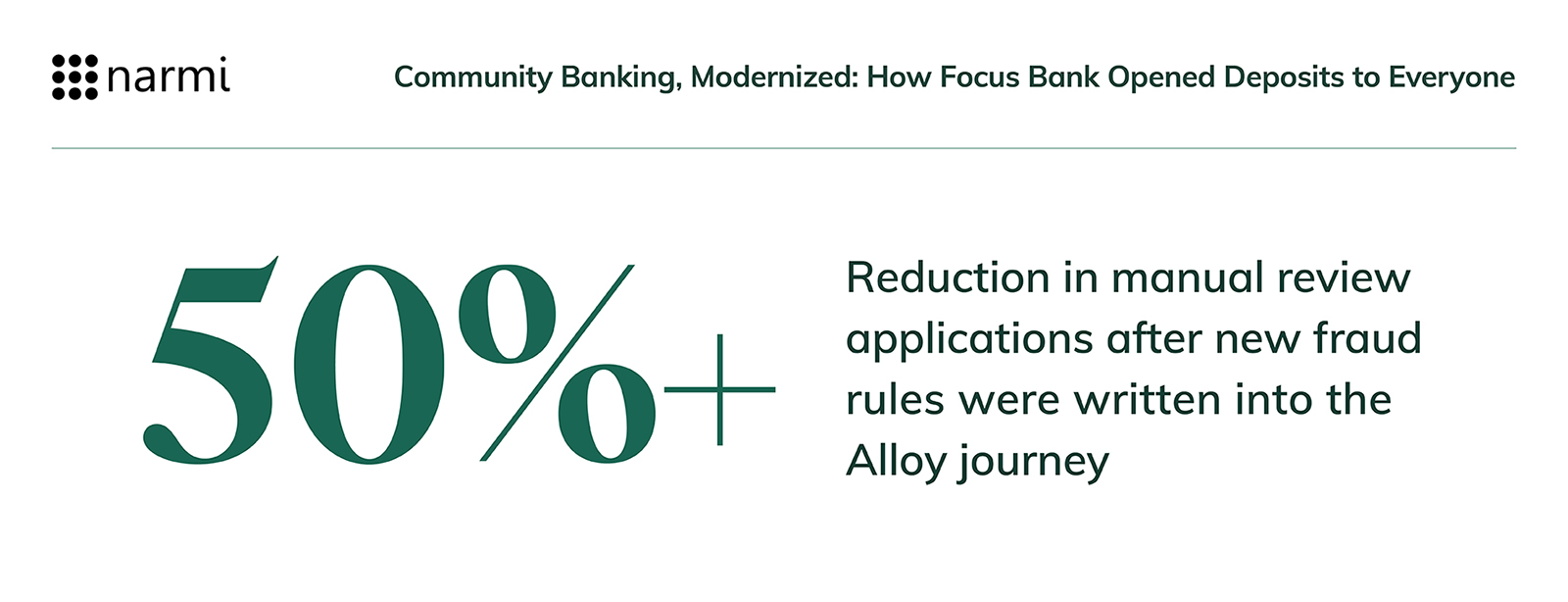

Narmi's integrated verification stack gave Focus Bank a layered approach that runs automatically in the background of every application. Alloy serves as the central decision engine, Socure provides identity intelligence, and NeuroID covers behavioral analytics. Together, they paint a complete picture of each applicant across multiple signals at once, giving the team the context they need to make informed decisions. When a fraud threat is detected, rules can be updated quickly in Alloy without rebuilding the process from the ground up. Within four months of going live, Focus Bank had already refined their Alloy journey, updating reason codes for national IDs linked to multiple DOBs and SSN frequency within Socure to better detect fraud before it reaches manual review.

Focus Bank's BSA team was involved from the start, helping configure the products, set up the compliance question series, and decide how verification should work for their specific exam requirements. That included a deliberate choice to retain ID collection through Alloy's selfie and facial recognition process. It's a step some institutions skip to reduce costs, given it’s often treated as an add-on, but Focus Bank, true to its client-first approach, chose not to compromise. Many institutions defer that investment until a fraud event forces the conversation. Focus Bank built it in from the start, a decision their BSA team made with regulatory exams in mind and one that puts them ahead of where a lot of institutions eventually land anyway.

The result, in Anna's words: "Your system is giving us a real total view of that particular customer. If they walk into the bank, we can visually see they match the ID. But we really don't know anything else about that person. Your system gives us that total view."

Focus Bank now has a digital account opening channel that reflects how they actually operate, supports their compliance requirements, and is already driving deposit growth. CD accounts are coming in from customers who couldn't have been reached through branches alone, and the team is thinking about how to deepen those relationships over time through debit card activation, mobile onboarding, and eventually mortgage conversations.

But for Anna and the team, this was never just about adding a digital channel. It was about proving that a community bank can offer everything a national bank or fintech can, and still pick up the phone.

"We may be an $880 million institution in Southeast Missouri and Northeast Arkansas, but we have the same products and services as any fintech or national megabank out there. We just offer it with a real person. Don't be afraid to do business with these community financial institutions. Banking has evolved. The geographical boundaries are gone. And when you call us, you're going to get a live person who can actually help."

GAFCU wanted to offer CDs in the CAO platform but didn’t want to have to manually send CD receipts every time an account was opened. This labor-intensive method inhibited staff from capitalizing on a channel crucial for deposit growth. Narmi's platform customizations provided a solution: automated delivery of personalized CD receipts to each account holder via email.

Asset Size: $300M

Location: Paramus, NJ

Products: Consumer Digital Banking, Digital Account Opening

GAFCU encountered difficulties promoting additional product offerings, particularly with their CD accounts. They came to Narmi for a solution that could help them effectively cross-sell their CD products.

Narmi's platform customization streamlines operations for GAFCU’s staff, and will enable GAFCU to significantly reduce manual efforts spent on tracking and sending CD receipts.

Grasshopper’s support team historically used Zendesk to manage their client support operations. However, ensuring client conversations on the Narmi support portal remained consistent with the conversations on Zendesk took valuable time away from their support team. Using Narmi’s platform customizations, Narmi built a full integration between Zendesk and the Narmi support portal, saving Grasshopper’s support team over 30 hours each week on manual tasks.

Asset Size: $820MM

Location: New York, NY

Products: Business Digital Banking

Grasshopper recognized the need to optimize their workflow by automating the connection between Zendesk and the Narmi messaging platform. This desire stemmed from a commitment to enhance operational efficiency and streamline processes.

Through this integration, Grasshopper can take full advantage of their existing tech stack. Reclaiming the 30 hours it took to copy messages from Zendesk to the Narmi platform allows Grasshopper’s support team to redirect their focus towards high-impact initiatives and delivering exceptional client experiences.

UFCU’s team was experiencing a high volume of applications that needed to be manually flagged, and they wanted to incorporate a tool into their risk management stack that could help relieve that burden. In partnership with Narmi, UFCU adopted NeuroID to automatically flag and decision for risky applications and send staff notifications when there are incidences of fraudulent activity. Now, UFCU’s staff can sit back and relax knowing that NeuroID is automatically decisioning on those risky applications, even when there’s a fraud attack.

“There were 33 applications that were declined outright on Sunday when otherwise it would have gone to Review or Accepted. This addresses Synthetic fraud which is difficult to track.”

- Russell Shugart

Asset Size: $4.5B

Location: Austin, TX

Products: Consumer Account Opening

UFCU was experiencing fraudulent applications moving to “review” or “approved” status. These applications required constant manual review, causing their staff to be bogged down and overwhelmed when there was a fraud attack.

With NeuroID catching risky applications and automatically decisioning them, UFCU’s staff saves hours every week. In the short time since implementation, Russell calculated that NeuroID saves more than 40 hours a month in manual review time and helps UFCU avoid charge-offs averaging $400 per fraudulent account. With Narmi’s close integration with NeuroID, UFCU can more reliably trust application decisions, giving them a safety net when experiencing intense fraud attacks.

.jpg)