If this past year taught us one big lesson, it’s that the future is anything but predictable. And yet even in uncertain times, there are digital banking trends on our radar we’re anticipating will continue to grow in relevance in 2021.

The tumultuous events of 2020 upended normal life for nearly everyone in the world. With the ground shifting underneath their feet, many people have had to make dramatic changes in the way they spend and save – including reevaluating their relationships with the brands they were once loyal to. This is true for both retail consumers and business owners.

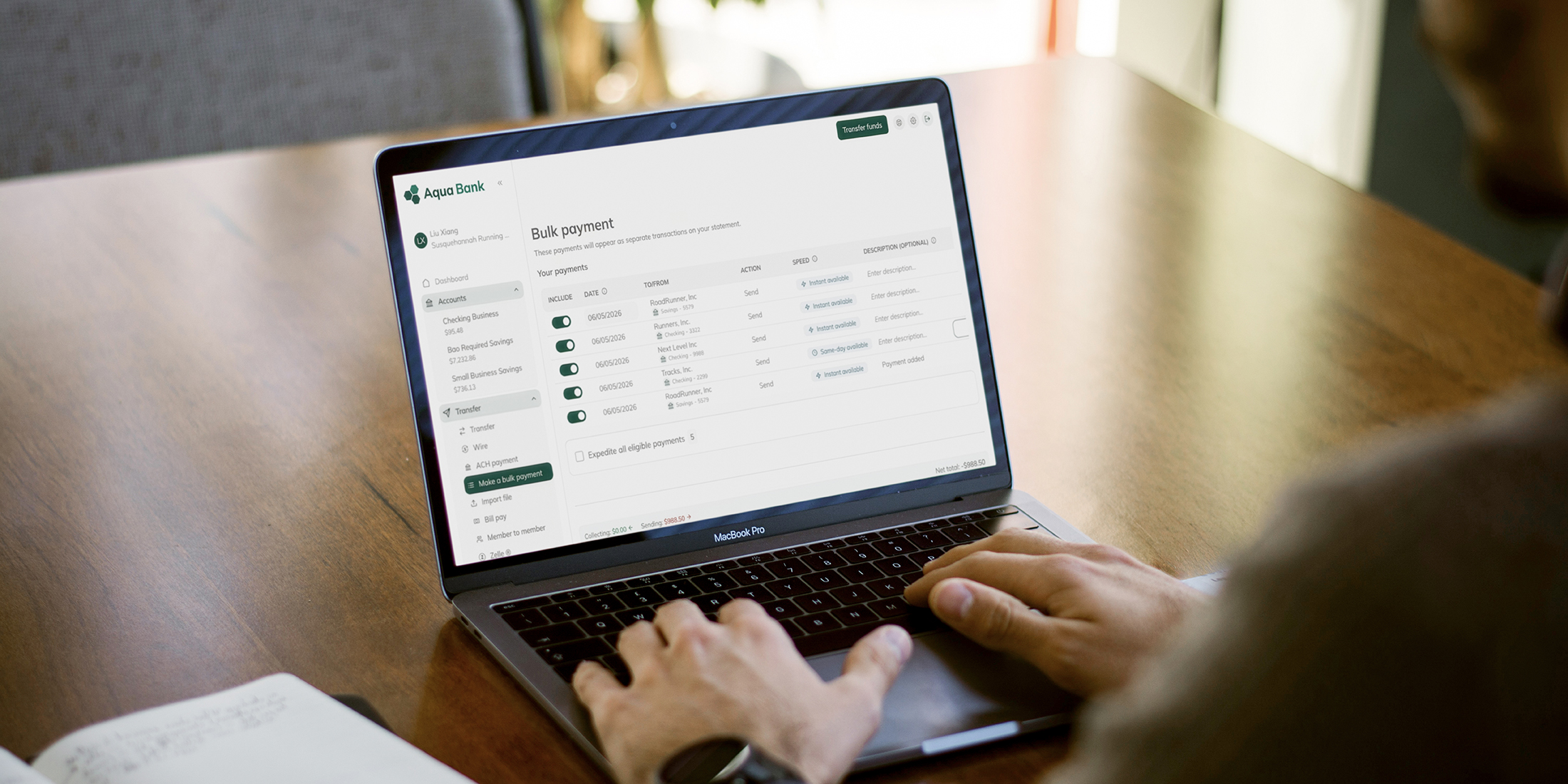

Virtual and mobile-first solutions have gone from novelty to necessity. Consumers demand better user experiences and technology that reduces friction in their daily lives. For banks and credit unions struggling to overcome their technology gaps, consumer satisfaction dropped significantly in 2020, with the overall banking industry seeing a 2.5% drop in customer satisfaction.

The ability to quickly and easily open new accounts was a particularly tough struggle we heard from many financial institutions in the latter half of 2020. Limited access to branches coupled with stay-at-home orders and anxieties of personal safety left those without a Digital Account Opening solution in the lurch. Many missed key opportunities to open new accounts and earn deposits.

Last year’s Paycheck Protection Program loan distribution served as a valuable test of the relationships businesses have with their financial institutions. During the rollout, many small- and medium-sized businesses – which make up a staggering 99.9% of all businesses in the US – had much better experiences working with community banks and credit unions for assistance than they did from larger banks.

In fact, community banks and credit unions were responsible for almost all of the PPP credit provided to small businesses in the first month. For those financial institutions prepared to serve the needs of businesses seeking assistance, these loans also provided an opportunity to introduce products and services to a new, highly receptive audience.

The most successful financial institutions were able to grow deposits, open accounts, and bring new business clients into their communities. The work to rebuild the U.S. economy with the promise of a post-COVID future on the horizon will shape much of 2021, with small- and medium-sized businesses playing a central role in the economic turnaround.

The exact shape of the "next normal" is still out of focus, but we can clearly see a renewed push for banks and credit unions to fully "go digital." But in this time of increased demand for well-designed digital experiences, many financial institutions are struggling to keep up. All too often, the culprit is heritage technology.

In order for financial institutions to stay competitive and provide the services their depositors need, it’s crucial to eliminate legacy bottlenecks – the biggest of which being Core Banking Systems that limit access to your data.

Even if 2021 isn’t the year your financial institution can switch core providers, we believe the industry swing towards openness and accessibility will make it easier to work around the limits of heritage technology. Our own efforts to further openness led us to developing the Narmi Application Framework and AppXchange – empowering our customers to quickly build and launch features and integrations their customers expect. This model, and the growth of other middleware points of integration, will only increase in 2021.

The choice then for core providers will be to invest in opening access to data and embracing contemporary API developing channels or face growing irrelevancy.

Over the past decade, digital-only neobanks have had a meteoric rise in popularity in the E.U. and here in the U.S. By offering a lightweight set of features designed for an active mobile lifestyle and eliminating unnecessary fees, these branchless banking platforms have been able to appeal to a large swath of the retail banking and small business segments.

However, very few of these new companies have been organized as chartered financial institutions, oftentimes relying on established financial institutions who’ve leveraged their own charters. But as the banking industry at-large moves closer to true openness in banking, we expect to see more traditional banks spin up digital-only retail and entrepreneur-focused offerings of their own.

With the recent announcement of BBVA shutting down Simple and Azlo prior to their pending sale to PNC Financial Services Group, it’s likely we’re already starting to see the neobank bubble burst. In the case of Simple, the early entrant fintech that revolutionized retail banking with beautiful digital-only experiences and excellent customer support, many of their early cutting-edge product differentiators are now becoming ubiquitous among banking platforms.

In 2021, we’re predicting additional closures like this as established banks and credit unions accelerate their digital transformations in the wake of COVID-19. But, this is hardly the end of challenger digital-only banks. The most successful will continue to push the banking industry forward with modern approaches to institutional roadblocks.

One trend that we’re keeping a close eye on as we head into 2021 is the growing number of financial institutions leveraging their charters and current technology stack to spin up digital-only brands.

This practice was gaining popularity amongst forward-thinking banks before COVID-19 as a way to stay competitive with the rise of fintech and challenger banks. Brand building is a powerful way for established financial institutions to identify the needs of niche audiences and offer a unique branded experience specific to that market. Considering the prohibitive obstacles that come in trying to secure a new charter, banks are uniquely positioned to cash in – particularly those with heritage offerings looking to appeal to a new customer base.

We believe this is an excellent opportunity for institutions to find new ways to differentiate themselves. Given the increased importance of digital channels, the ability to quickly invest in new technology is crucial for 2021. In some cases, we’ve seen institutions establish multiple distinct banking brands all leveraging one charter, essentially shoring up any gaps in their market that would be easy pickings for neobank challengers.

Credit unions and community banks are finding themselves in a difficult spot, knowing they need to grow their offerings and cross the "virtual divide" in order to better connect with their customer and member base; all while handicapped by the limited access to in-person interactions.

Prior to COVID-19, the physical branch was the primary experience-based touchpoint for customers and members. A location where depositors could have their individual needs assessed, and a personalized financial plan could be developed. This, of course, is no longer possible for many financial institutions forced to rethink the branch model. Some are even seeing new opportunities for branch banking only made possible with the increased adoption of open banking principles.

We believe that in 2021, the industry will continue to see a rise in quality third-party vendors specializing in personalized financial health solutions. These forward thinking vendors can help financial institutions access more of their core data – empowering them to become stronger partners in the financial health of their customers and members.

For more info on choosing the right partners to assist in the financial health of your members and customers, watch our webinar on growing your share of wallet with 3rd party vendors.

Of all the major shifts brought on by the pandemic, the transition to a primarily remote work environment for employees might have the most lasting impact on digital banking.

A strong remote workforce has long eluded the banking industry, with fears around data security and decreased productivity being the largest and most lingering concerns for financial institutions. For the most part though, institutions have been able to adapt to an indefinite work-from-home workforce without any major hiccups. Cloud-based banking, access to VPN licensing, and large-scale investments in technology have largely made these successful transitions possible.

Banking customers and credit union members have also had to adapt to new digital channels and virtual workarounds to things they would typically take care of at the branch. With an uptick in activity and transactions as users move from physical to digital channels, financial institutions must be quick to react to issues that arise.

Digital experiences can’t directly replace in-person interactions, but improved admin platforms that offer real-time chat support and screen emulation can vastly streamline the support process. Any friction that can be removed around internal systems will positively impact operational efficiency, and give remote workers the support they need to do their best work.

Even with 2020 solidly in our rearview mirrors, many of the factors that made it a tumultuous year are still with us. However, we enter 2021 with resilience, fortitude, and systems in place to help us adapt to whatever comes next.

We don’t yet know what this year holds, but we do know that improving project management will help us build agile teams. We know to anticipate change. Financial institutions historically haven’t had to change their ways very much, often wearing their immutability as a badge of pride. And yes, stability is an expected and admired quality in a financial institution. But so too is an ability to provide amazing services and offer products people need during a time of extreme difficulty.

The forward-thinking banks and credit unions supporting openness and prioritizing thoughtfully designed technology are those who will see growth and serve their communities well when the next unpredictable event happens. That we can count on.