For the last two years, the assumption in the industry was that it would take some time for the FedNow Service to approach the RTP network in terms of volume, limits, and general maturity. But looking at FedNow performance data from 2025 confounds that assumption: the network is indeed reaching maturity, but much faster than originally conceived.

We’re also seeing a payments market driven by what entities settlements occur between: big banks are, expectedly, seeing high volumes within the RTP network, while FedNow is quickly emerging as the “lingua franca” network for financial institutions of all sizes, and fast becoming activated for high-value commercial settlement.

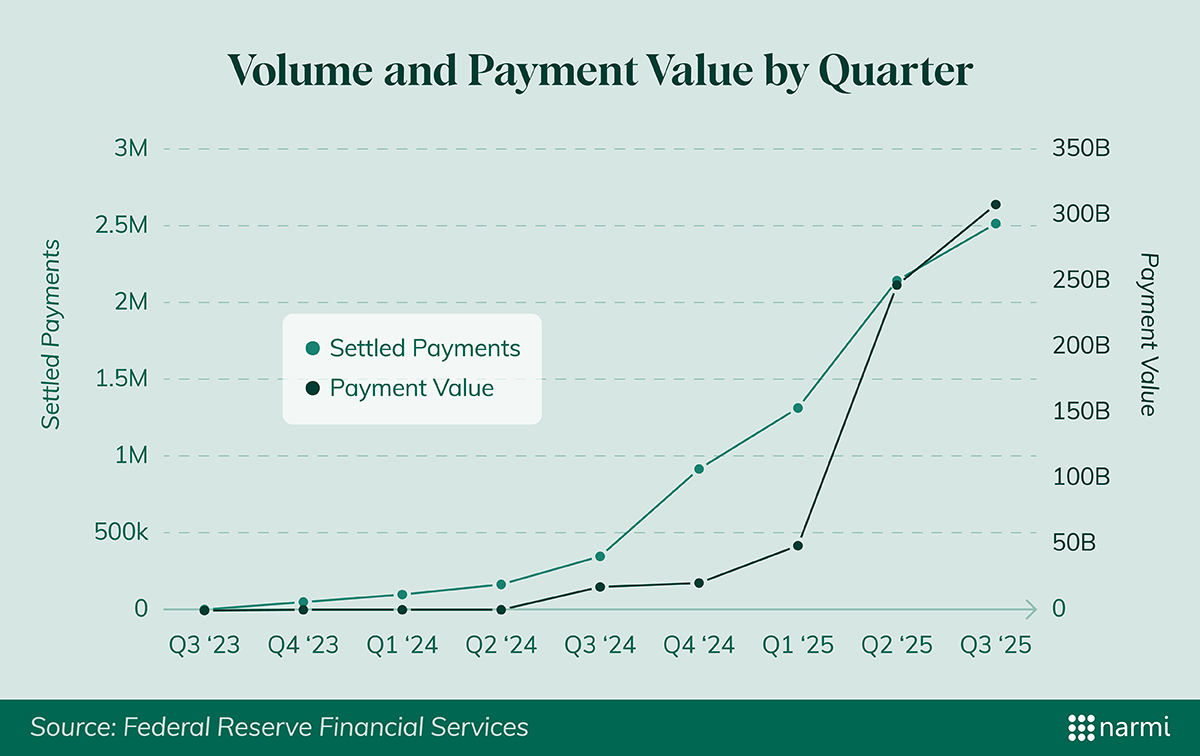

The headline metrics for FedNow’s 2025 show a maturation of the network and a marked “hockey stick” trend in its usage:

While the volume growth is steady, the value throughput is startling. To put Q425’s $250 billion figure in perspective: it represents over 50% of the total value processed by the mature RTP network in Q2 2025 (the most recent quarter for which we have official published data).

For a network that is effectively two years old to be moving more than half the dollar value of an incumbent that has been live since 2017 is a signal that should not be ignored.

The most remarkable data point in the 2025 report is the average transaction value seen on the FedNow network. Average payment size currently sits at approximately $100,000.

This is not P2P traffic. You don’t send $100,000 to split a dinner bill. Even in the absence of more granular data about the nature of these payments, we can note that this average transaction value is remarkably high, and even more notable given how quickly this pattern of behavior in the payments landscape has emerged – proof that organic experimentation with the FedNow network is giving financial institutions the confidence it can accommodate these kinds of high-value settlements.

Contrast this with the RTP network, which processes ~100 million transactions per quarter compared to FedNow’s 2.5 million. RTP touts a 40x higher volume of individual payments, but FedNow’s value-per-payment is roughly 25x higher.

RTP’s average of $4,000 per-payment – that figure itself up significantly from previous reported quarters – is more in line with what we might expect from an instant payment network. What is driving this sharp discrepancy between the two networks? Whatever the reason, it seems clear that FedNow is becoming trusted for high-value, balance sheet-relevant settlements, with less small-dollar penetration.

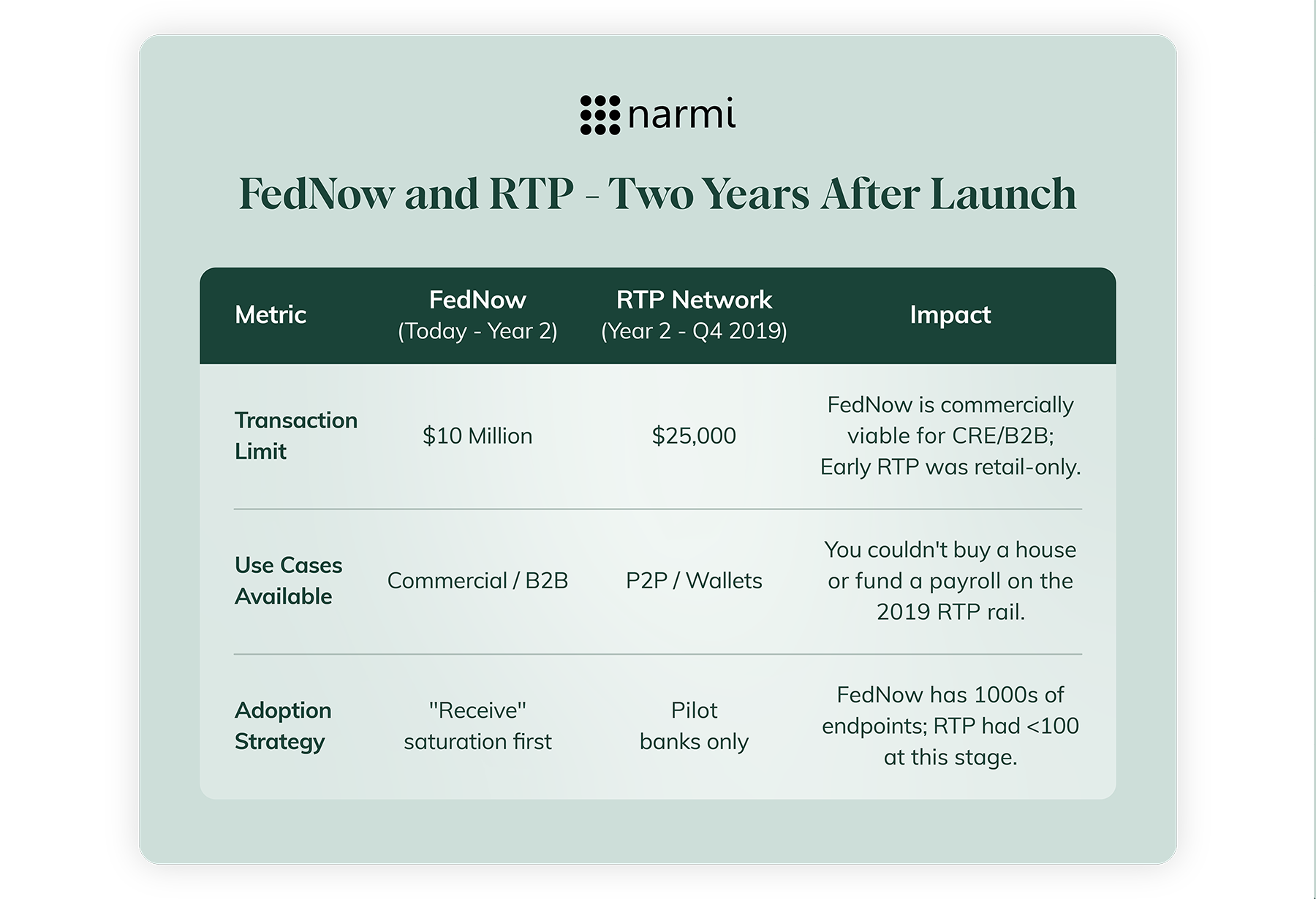

Skeptics often point out that FedNow’s volume (8.4 million payments in 2025) is low. But to fairly judge its trajectory, you have to compare it to where RTP was at the same stage of maturity.

When we look back at the RTP network two years after its launch (Q4 2019), the difference in commercial viability is stark.

This comparison highlights why FedNow’s adoption feels different: the rails are open for serious business much earlier in the lifecycle. To be sure, much of this is due to a “second mover” advantage: RTP was able to evolve organically without much competition in the banking instant payments market, and FedNow was able to benefit from the infrastructure and usage criteria that RTP had developed since its inception.

But this takes nothing away from the success FedNow has enjoyed in its short time: we can take the quick progression of the network as a success indicator, and a validation that the banking sector was in need of a solution for players of all sizes.

Despite the bullish value numbers, the 2025 data exposes a persistent bottleneck: the "Send Gap."

Processing $850 billion on just 8.4 million transactions indicates a highly concentrated user base. Thousands of financial institutions are connected to receive payments; a defensive necessity. But the operational capability to originate payments remains rare.

This is the next frontier. The infrastructure is built, and the limits are commercially viable. The banks that win in 2026 will be the ones that move beyond passive connectivity and build the products that allow their clients to actually hit "send."