The FI’s central role as a business banking provider may not survive without a reinvented digital business banking experience and payments infrastructure. A modern, integrated cash management experience builds up FIs as competitive business banking service providers, sets them apart from peers without modern digital and payments capabilities, and counters the direct threat to the customer relationships posed by fintechs — FIs are not destined to just hold deposits and process payments. FIs’ relationships with business customers should be so strong and digitally engaging that even in the presence of intense competition, they always come out on top as customers’ primary business FI.

FIs as a whole should strike back at fintechs by excelling at their strengths, enhancing the experience in their direct channels, and complementing software and services that meet other business needs. FIs should perform uniquely well with modern payment capabilities, enriched reporting and analytics based on their first-party data, and tight control over risk and compliance. FIs with dated or generic digital business banking and payments capabilities will fade into the background as those that plan furthest ahead capture the market.

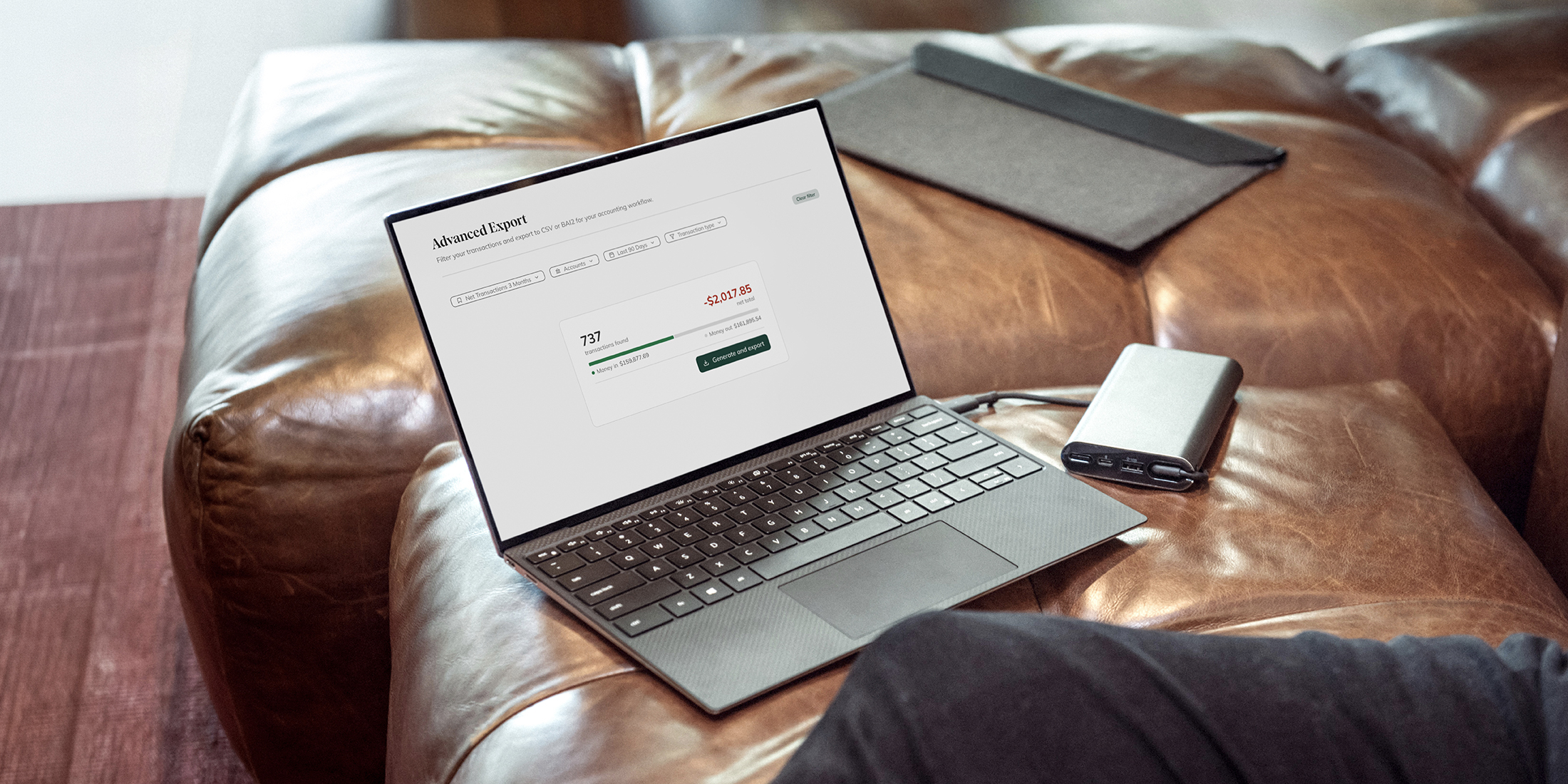

FIs that embrace their fundamental strengths as licensed institutions should over time make bigger plays with feature-rich, highly integrated digital business banking platforms. Recent data on features community FIs offer to small business customers suggests that treasury management (offered by 69% of respondents), integration with accounting systems (61%), and digital deposit account onboarding (51%) are table stakes. Real-time payments (36%), invoicing (17%), and cash flow forecasting differentiate them (6%).

Business customers universally demand digital features that help them improve their cash flow and manage their banking needs efficiently and effectively. And all want feature parity and seamless handoffs between mobile and online banking. Business banking users are consumers, too, and will expect a seamless experience interacting with other products they own. But there is no one-size fits all in business banking: Customer needs and their sophistication can be extremely diverse. Some large business customers export financial data via CSVs and submit payments in batch files. A sole proprietor may want instant payments and wires with a click or a tap. Business products and services tailored to different segments’ needs will be distinct; relationship management and self service must reflect those differences.

Massive changes to core payments and customer expectations impact the digital business banking experience and what FIs should need on the back end. There’s no patience anymore for waiting for money to arrive when customers think that it can be instant, either through a fintech P2P app or through Zelle. Immediacy and irrevocability has value for all parties for liquidity management and certainty. Instant payments also have many specific applications in B2B payments, person-to-business payments, business-to-person payments, and account-to-account transfers. These use cases are largely unexplored, especially by FIs.

An FI’s place in the payments value chain suits it uniquely to compete on faster and instant payments, even with fintechs that run closed-loop payment systems. It’s especially the case when an FI’s primary payment processor connects directly to the Fed. With a direct Fed connection, FIs simplify their bank relationships, minimize their processing costs, and mitigate the risks of having multiple intermediaries involved in a transaction. They can pass the cost savings through to their customers, or expand their margins by monetizing payment speed and selling analytics based on data that’s proprietary to the FI and customer.

Fed data suggests that US businesses most commonly see top payments pain points as fees (48% of respondents), security issues (32%), and speed or timeliness (32%). Instant payments will address these concerns, if FIs implement them thoughtfully and effectively: They may revisit fee structures and shift charges for payment processing to faster payments and more complex payment-related services. To address security, they may put in place modern account takeover (ATO) protections, while instant payments eliminate pull-payment fraud. Instant settlement removes concerns over timeliness, as long as counterparties send and receive on the same network.

FedNow isn’t a novelty anymore: The network has been live for a year and a half now, and has over 1,600 FI participants, up from 35 early adopters. Soon FedNow will be a must-have for FIs to be competitive in payments. It’s increasingly relevant to business customers as the Fed has raised and plans to raise again the network limit on value per transaction, as business transactions become a larger part of the payment mix.

The banking industry overall is still testing the waters. Bankers tend to agree that there’s not much risk to receiving instant payments, and that has played out in FedNow’s growth. But in many banker’s minds, there is a lot of risk in sending instant payments. Modern risk mitigation tools derisk instant payments, and even make them less risky than ACH. Fraud rates suggest that other rails have much bigger fraud problems. FIs should get used to the idea that instant payments are not going away, that their competitors use them, and that to be competitive, they will also need a comprehensive instant payments feature set.

Business banking is an enduring bright spot for regional and community FIs, and they should lean into digital self-service and payments modernization. Strategically, digital business banking should raise customer lifetime value. It enhances relationship depth and drives direct revenue from services that customers are willing and able to pay their FIs for. Tactically, digital business banking should transform basic account management and payment initiation into comprehensive treasury management, including integration with customers’ other tools. Branded digital business banking capabilities should compete favorably with FI and fintech alternatives. The result will be a pronounced increase in customer engagement and loyalty to the FIs for high-margin and profitable, high-volume financial products and services.