When it comes to digital account opening, the right product at the right time is not just a nice-to-have. It is the difference between a completed application and a lost member. That is why Narmi has spent time building what we call the personalization stack: a coordinated set of controls that ensure every applicant sees exactly the products they should, and nothing they should not. With Cross-Product Validation newly available, the final piece of that stack is in place.

Most account opening platforms present every applicant with the same product catalog. For financial institutions, this creates a set of compounding problems that are easy to overlook until they show up in conversion data.

An existing member trying to open a secondary account gets shown membership share products they already hold. A student applying online sees commercial products irrelevant to their situation. A new applicant eligible for a bundle has to find and select each product individually, introducing friction at exactly the moment they are most committed.

The result is user abandonment, confusion, and in financial institutions specifically, a growing backlog of duplicate and redundant accounts that staff are left to manually clean up. Some institutions have disabled their existing member digital onboarding flow entirely to avoid this experience, routing members back to branch visits rather than letting the digital channel handle what it should handle automatically.

Narmi's personalization stack addresses each of these failure modes by using the applicant’s PII to deeply understand who the applicant is and where they are in their journey, ultimately tailoring products they have access to based on that data.

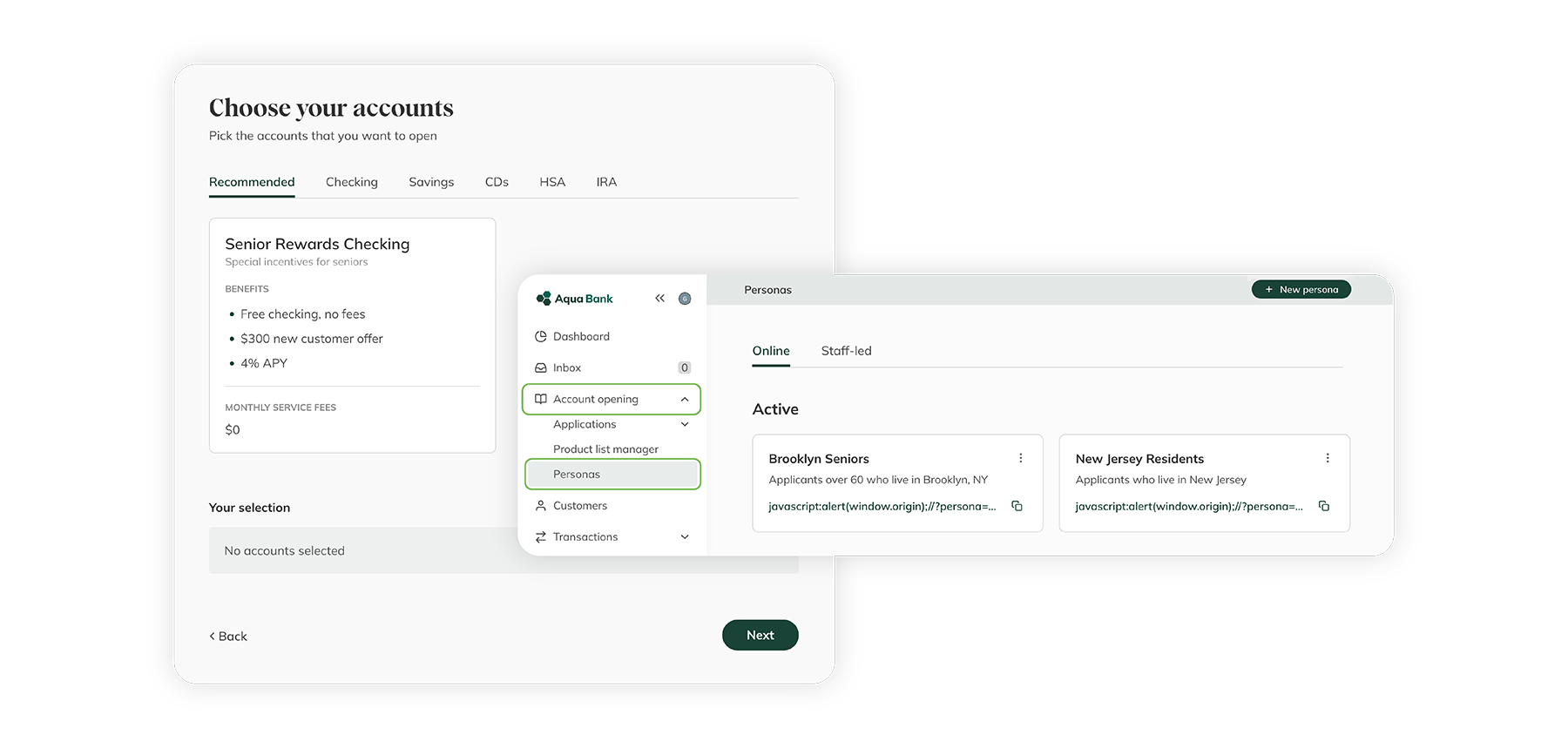

The foundation of personalized product selection. Personas allow financial institutions to define applicant segments by URL parameter, demographic attribute, membership type, campaign source, or any combination, and automatically filter and pre-select products for each segment. A student applicant coming through a campus partnership link sees a curated set of student products. A business applicant sees the commercial suite. A returning member picking up a saved application picks up exactly where they left off.

Personas are configured in Command and apply across Consumer Account Opening (CAO) and Staff-Led Account Opening (SLAO), meaning the same logic that governs self-service digital applications can inform branch-assisted flows as well.

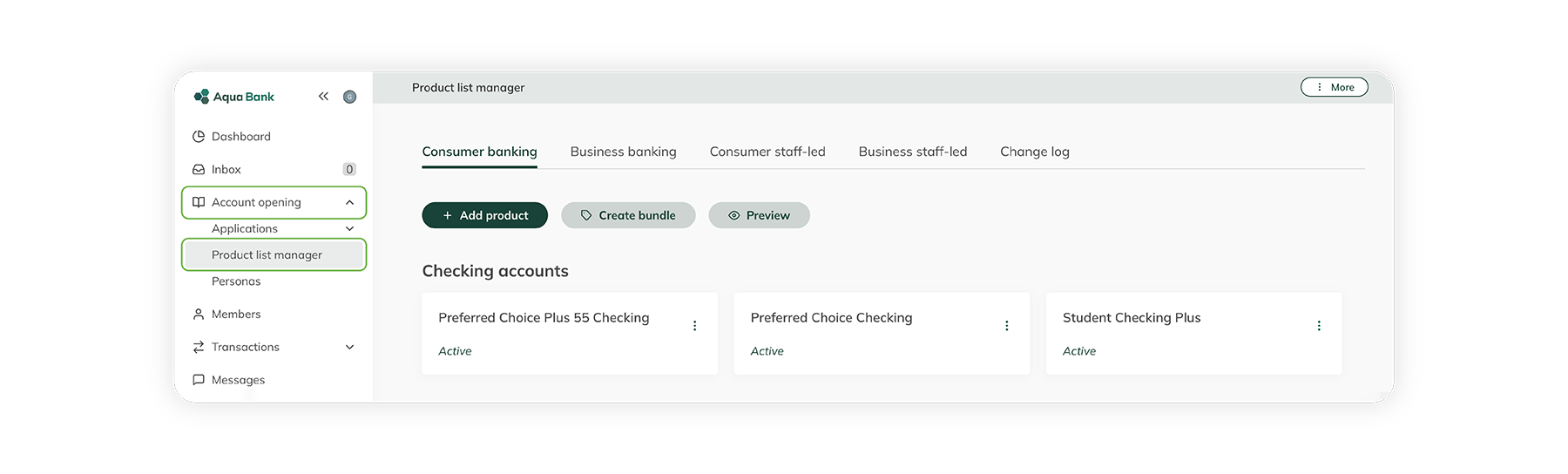

If Personas define who sees what, the Product List Manager defines what is available to be seen in the first place. It is the centralized admin interface for configuring, previewing, and managing every product offered through account opening, with full audit logging, real-time preview, and self-service controls that do not require a support ticket to update.

Before the Product List Manager existed, changes to product availability meant back-and-forth with implementation teams. Now a digital strategist at a credit union can adjust their product catalog, preview exactly what an applicant will see, and deploy changes without engineering involvement. The full audit trail means every change is logged and attributable, an increasingly important requirement for institutions with compliance and governance obligations.

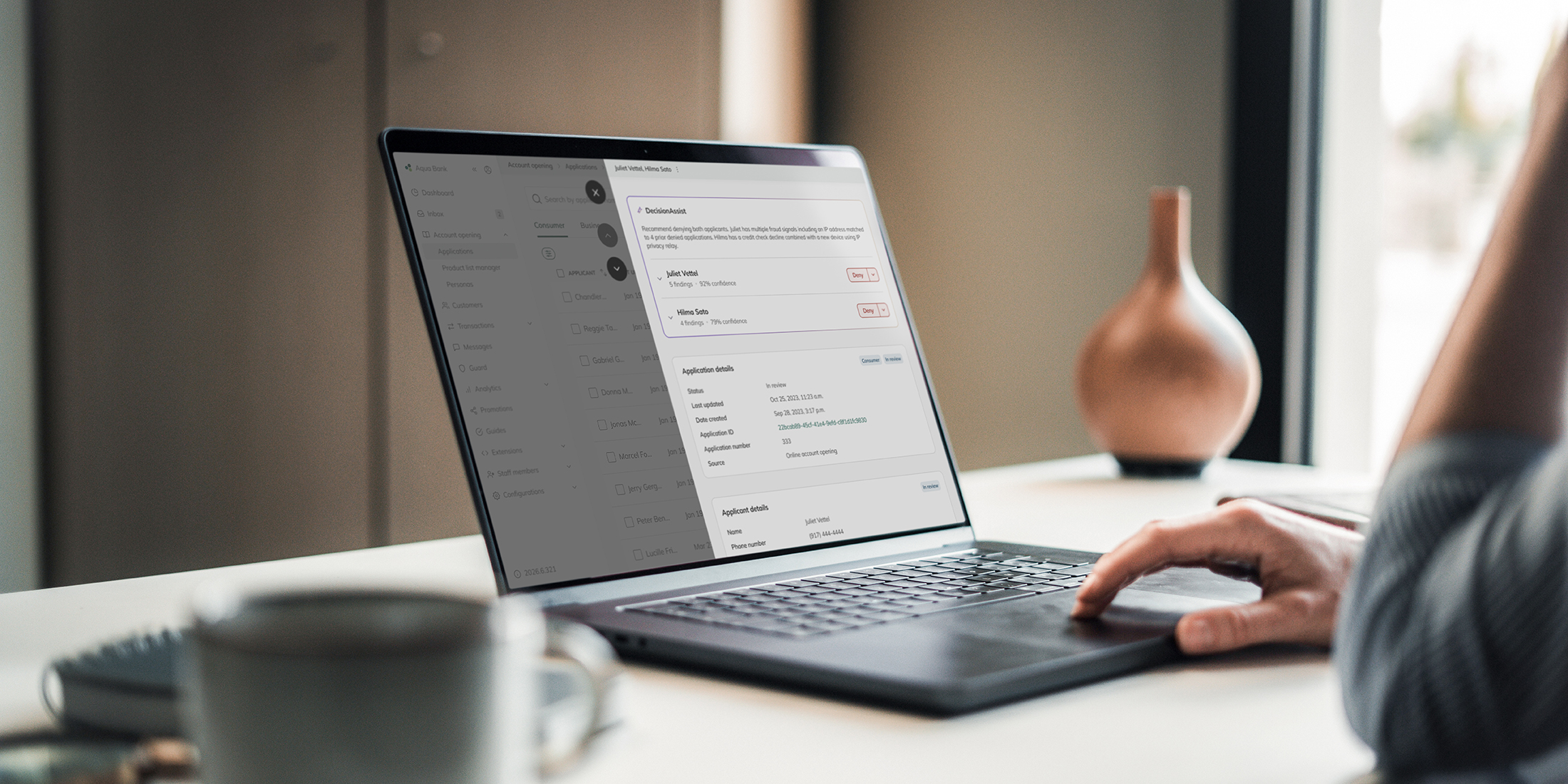

This is the newest addition to the stack, and the one that solves the problem institutions have been working around for years.

Cross-Product Validation introduces configurable if/then and either/or rules that control which products an applicant sees based on what they already hold. These rules are core-agnostic and apply in real time during the account opening flow, automatically suppressing or surfacing products based on the applicant's existing relationship with the institution.

The use case that prompted the feature is straightforward: a credit union wants to show a CD only to applicants who already have a checking account. Without Cross-Product Validation, there is no mechanism to enforce that logic digitally. Staff have to catch it manually, or applicants end up in inappropriate product flows. With the feature enabled, the rule is defined once and enforced automatically across every applicable session.

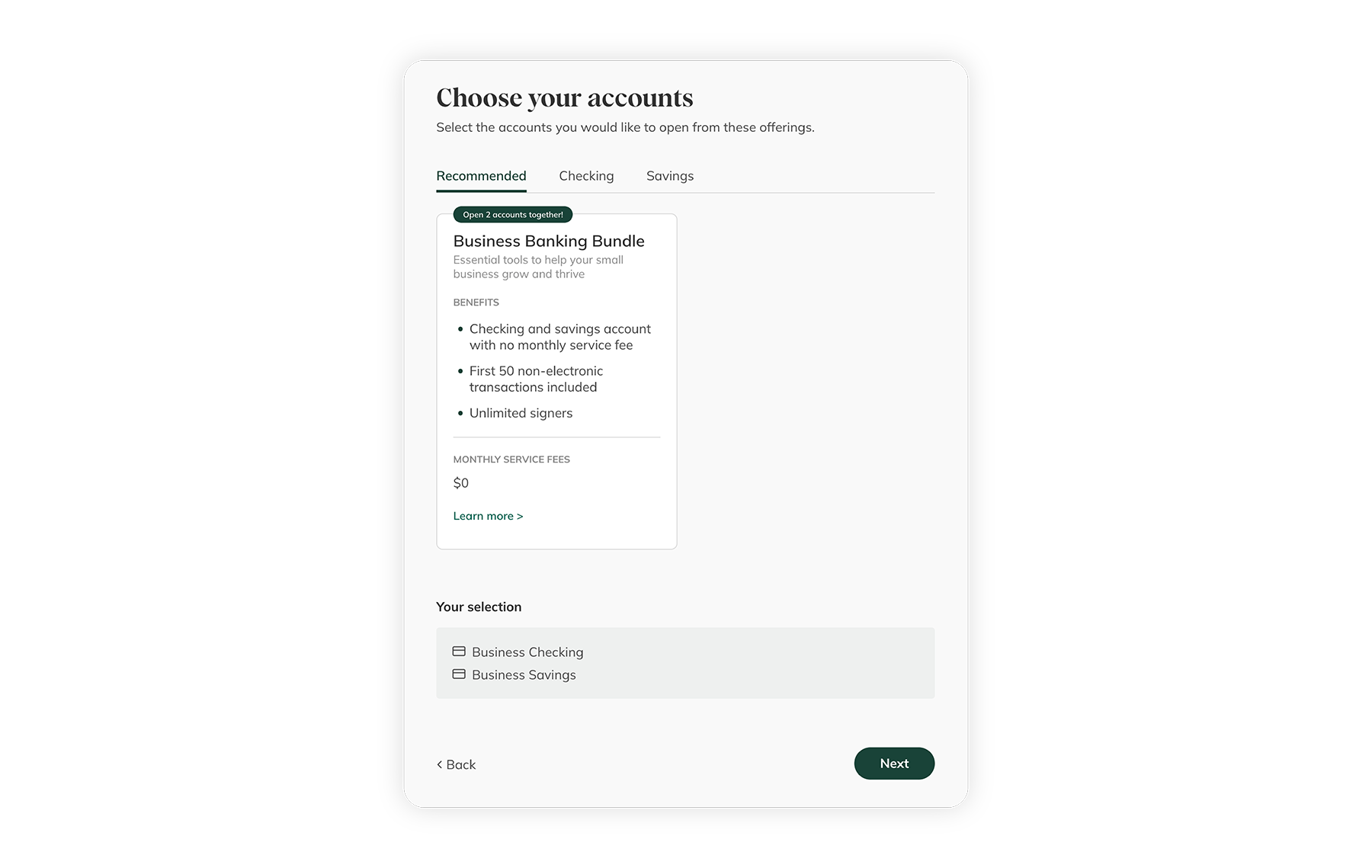

The complement to Cross-Product Validation. Where validation rules prevent applicants from seeing products they should not, Bundles make it easy to present products that belong together as a single, selectable card.

A Checking + Savings bundle, for example, surfaces as one option rather than two separate line items. The applicant selects it with a single click, both products enter the application together, and the institution increases multi-product acquisition without adding friction. Bundles are Persona-compatible, so a bundle visible to one segment can remain hidden from another, and they apply across CAO and Business Account Opening (BAO).

Community banks and credit unions operate with product complexity that the largest digital-native banks have designed around by limiting their catalogs. A credit union might have a Personal Membership Share, a Student Membership Share, a Senior Membership Share, and a Community Membership Share, plus checking, savings, CDs, money market accounts, and credit products across multiple tiers. Managing which applicant sees which product, and ensuring that existing relationships are respected throughout the flow, is not a simple problem.

Narmi's personalization stack was built specifically for this complexity. New applicants see a clean, relevant product catalog shaped by who they are and how they arrived. Existing members are recognized and shown only the products appropriate for their current relationship. Duplicate account creation is blocked at the rule level, not caught after the fact by staff. And multi-product relationships are encouraged from the very first session.

The goal is not to simplify what financial institutions offer. It is to make the full depth of that offering navigable, relevant, and conversion-optimized for every applicant who walks through the digital door.