To thrive in the age of accelerated digital, modern financial institutions need access to actionable business intelligence. It’s what allows them to unlock the full power of their data and make informed decisions. But, many don’t know where to begin or how exactly to work with their data to their optimal benefit. Without leveraging this information, businesses can easily fall into the same patterns that can stunt growth–failing to attract new customers and even leaving themselves open to security risks.

Luckily, there are intelligent and scalable ways institutions can access and make sense of their data, allowing them to spot trends and extract insights that drive innovation and inspire creative solutions.

In this post, we’ll explore some key practical applications of data analytics for financial institutions, and showcase the power of insights gleaned from business intelligence solutions.

Business intelligence is the practice of leveraging data in order to make informed decisions with regards to how a product or service is being used. Data gives insight into user demographics, habits, preferences, and more. By studying it, businesses can evolve and pivot to better fit their users’ needs, as well as how to prioritize the information in a way that benefits the health and growth of a business.

Many financial institutions face common challenges when it comes to turning their big data sets into actionable business intelligence. Without robust in-house expertise and support to build the necessary dashboards and run queries, many institutions are instead forced to rely on canned reports that can’t be customized.

In an informal poll from Narmi, leaders described accessing their data as “very manual,” with nearly 70% describing a cumbersome process that required them to exit workflows. Other times, data may be siloed in disparate sources, leading to an incomplete picture of user activity. Safety is also a concern, as the data often includes sensitive personal information that must be handled accordingly. These challenges can prove frustrating. There’s consensus that democratizing data is a priority, but many credit unions and banks are at a loss when it comes to making this a reality.

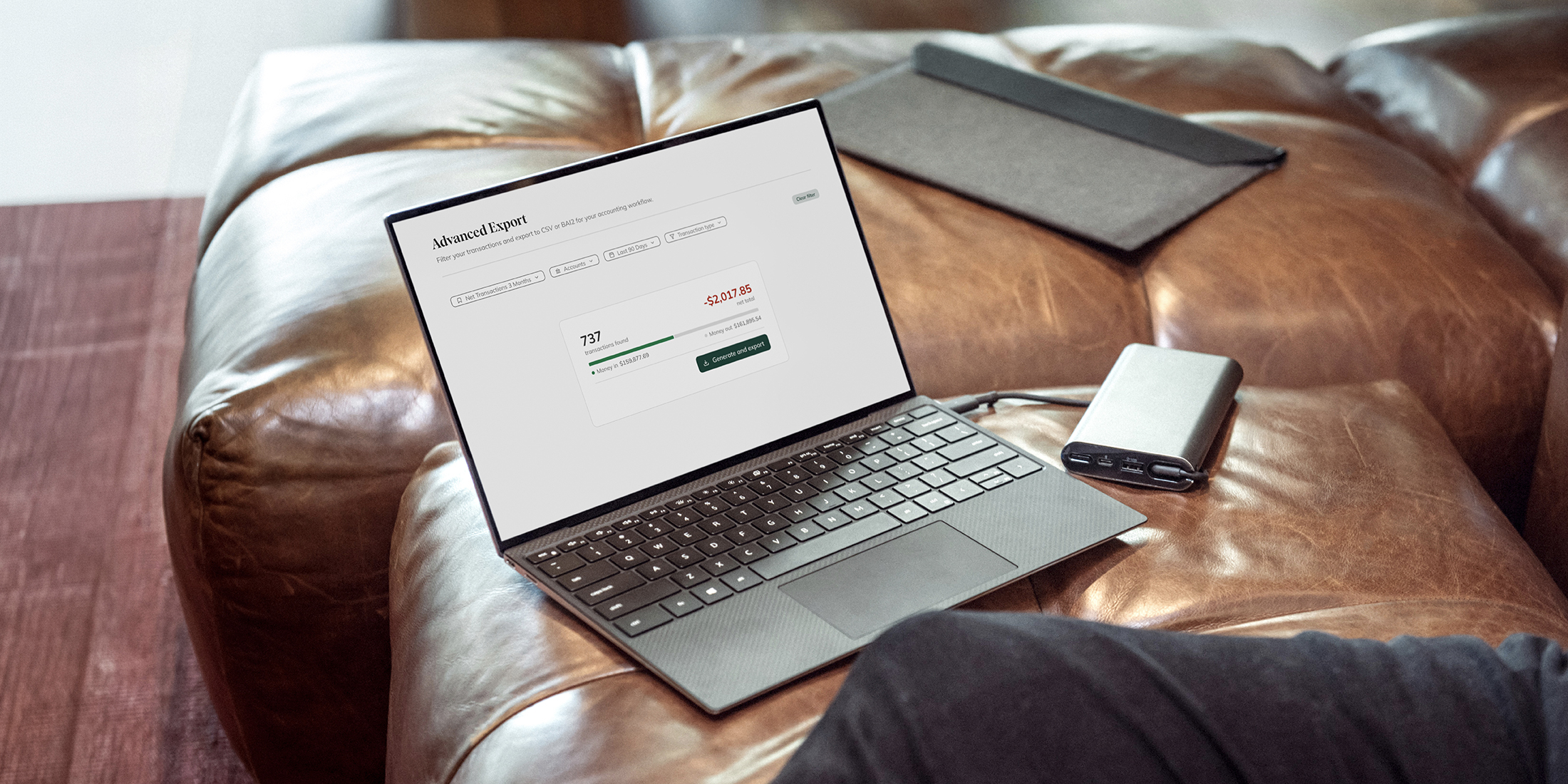

To address these common pain points around data analysis, we partnered with Sisense to develop an embedded business intelligence platform, Narmi Analytics.

Financial institutions have used business intelligence to navigate a number of challenges, from attracting new customers to maintaining security. Dashboards that are easy to customize and share across departments allow institutions to tailor their analysis and ask better questions of their data. And utilizing a solution like Narmi Analytics, our customers can filter by information type and visualize their data in bar graphs, pie charts, scatter maps, or whatever is most appropriate. These filters can also be layered for a truly granular look at data that takes into account all the factors that make up user behavior–unearthing new insights that lead to growth.

Here are just a few examples of how powerful business intelligence can help financial institutions from our recent Narmi Analytics webinar:

First and foremost, data can inform financial institutions about customer and member activity. Data can tell an institution where their users are located, which branches they’re visiting, how often they log into online and mobile banking, and a host of other information that can help institutions create and market products better.

But behaviors are never set in stone. Data can also keep banks and credit unions up-to-date on shifting trends as technology, banking, and the world at large. By asking the right questions of data, institutions can learn how to best adapt in the face of those changes.

Let’s say that, pre-COVID, data showed that the people logging in the most were between the ages of 22 and 44 years old, with users over the age of 44 as well as users under the age of 22 logging in less. One explanation for this trend could be that digital banking is more useful for that middle generation–old enough to need traditional banking services, but young enough to be tech-savvy. The older generation might have been more comfortable going to branches in person, while the younger was maybe not yet setting up accounts.

However, in 2020 and 2021, the login frequency of users spiked across age groups around March of 2020 as people stayed home during the pandemic, but still needed to manage their finances. In this instance, financial institutions would need to pivot to provide resources for especially the over 44 year old population that might be less comfortable navigating the digital space than others.

With Baby-Boomer-aged account holders accelerating into the digital space, banks and credit unions now had the opportunity to share with them all manner of digital products. They would also have the opportunity to develop new products for people of this age but tailored for digital and mobile rather than in-person banking.

Making informed business decisions is virtually impossible without knowing or being able to predict what users are doing. By mapping user behavior like spending habits, monthly and yearly patterns of spending, and more, financial institutions’ leadership teams can better plan for the future. This insight can inform future partnerships, and reduce uncertainty about which services will be most relevant and useful.

But to do that, they need to first know the basics about their users’ habits. Where are they spending their money, when, and how often? Narmi Analytics provides the option to see what your users are buying on a detailed level, including the places they shop, eat, and travel. You can even look into individual categories or add filters like age or location to see spending habits on a granular level to find unexpected ways to capitalize on these habits.

Once you know what peoples’ habits are, you can keep them engaged by leveraging products related to those habits. For example, if they’re traveling more, consider promoting travel integrations, such as Booking.com. If you notice customers are shopping at department stores during certain times of the year, consider implementing a cashback rewards system during those times. This will allow people to rely on their institution's services to help them handle everything from the routine chore of paying bills to significant transactions. Additionally, improvements here can also minimize operating costs, as online banking has been shown to be a cheaper service for institutions than transactions involving in-branch staff.

Digging deep into user behavior offers a wealth of marketing possibilities that might be totally unexpected, and a new collection of potential ways to connect with users in a way that makes them feel heard and seen. The more products an institution offers that feel relevant and useful to customers, the more likely they’ll be to turn to that financial institution to reap benefits.

Appealing to new customers can be a challenge for financial institutions, especially when it comes to offering relevant products that will make them want to open accounts. Having an account that reflects their financial needs is key, but without data, it’s impossible to tell what those needs are.

Certain account types resonate more with certain demographics. If those over the age of 30 are more likely to open “premiere checking accounts'' than those under 30, then the marketing of premiere accounts should reflect an over-30 demographic.

Location is also a key factor in attracting new customers, and a crucial factor when institution’s are deciding where to spend on marketing efforts. In this example, let’s take a look at a financial institution with locations in Norfolk and Chesapeake, Virginia. While these cities have similar populations, data showed that more accounts were opening in Chesapeake than in Norfolk. However, accounts in Norfolk were seeing more consistent funding with higher funding amounts.

Marketing new accounts in Norfolk, since people there were more likely to fund them, would lead to an increase in revenue for the Norfolk branch. At the same time, efforts in Chesapeake could be implemented to see why accounts were being opened, but not funded, and to see if there was a product better suited to the Chesapeake community. Cross-researching the account type with user ages would also yield information about which age groups were opening and funding accounts, determine patterns or correlations, and show how to better tailor marketing to those user bases for increased revenue in both locations.

Most banks and credit unions have measures in place to ensure suspicious activity that might suggest fraud and money laundering is monitored. For instance, while institutions have measures in place to note and investigate suspicious activity, sometimes smaller, more innocuous-seeming activities can slip through the cracks, or appear as non-suspicious even to a trained individual. That’s because information on the users and their activities is often incomplete and hard to find, which can lead to fraudulent activity remaining undetected because patterns are missed.

This data shows a list of users who have undertaken multiple cash deposits either at or just below the $10,000 limit. It can be filtered to see their location, as well as their spending habits to gauge the suspicion level of the activity.

Data can also track new account creation, and alert when accounts are opened in suspicious or potentially fraudulent ways. For example, if there’s a spike in new account creation centralized to a specific location over a short period of time, this may indicate fraudulent activity.

Finally, data can keep financial institutions abreast of new fraud trends as technology evolves. By tracking how and where fraudulent accounts or actions are being made, financial institutions can implement smarter safety protocols where needed. What’s more, the data provided by Narmi Analytics can also provide context for these trends that can lead to even larger changes to prevent criminal activity.

Asking the right questions about data is crucial to the growth of any institution. But having access to the right data analysis tools is equally important and can even lead to bigger, better, and deeper questions that will push for growth in even more directions.

In order to harness the power of data, financial institutions must first put their data front and center, making it a priority that informs all of their decisions. Narmi Analytics is a powerful but approachable tool that even the busiest of leaders and teams can use easily, and drill down to unlock a trove of useful information that just might transform their institution.

Narmi Analytics, powered by Sisense, provides customers with the opportunity to ask the most complex of questions, but still get straightforward answers to inform intelligent, data-driven decisions.