Americans now owe about $257 billion in personal loan debt, the highest figure in nearly two decades of available data. That figure is a 4.5% increase year-over-year, up from $246 billion last summer, according to LendingTree.

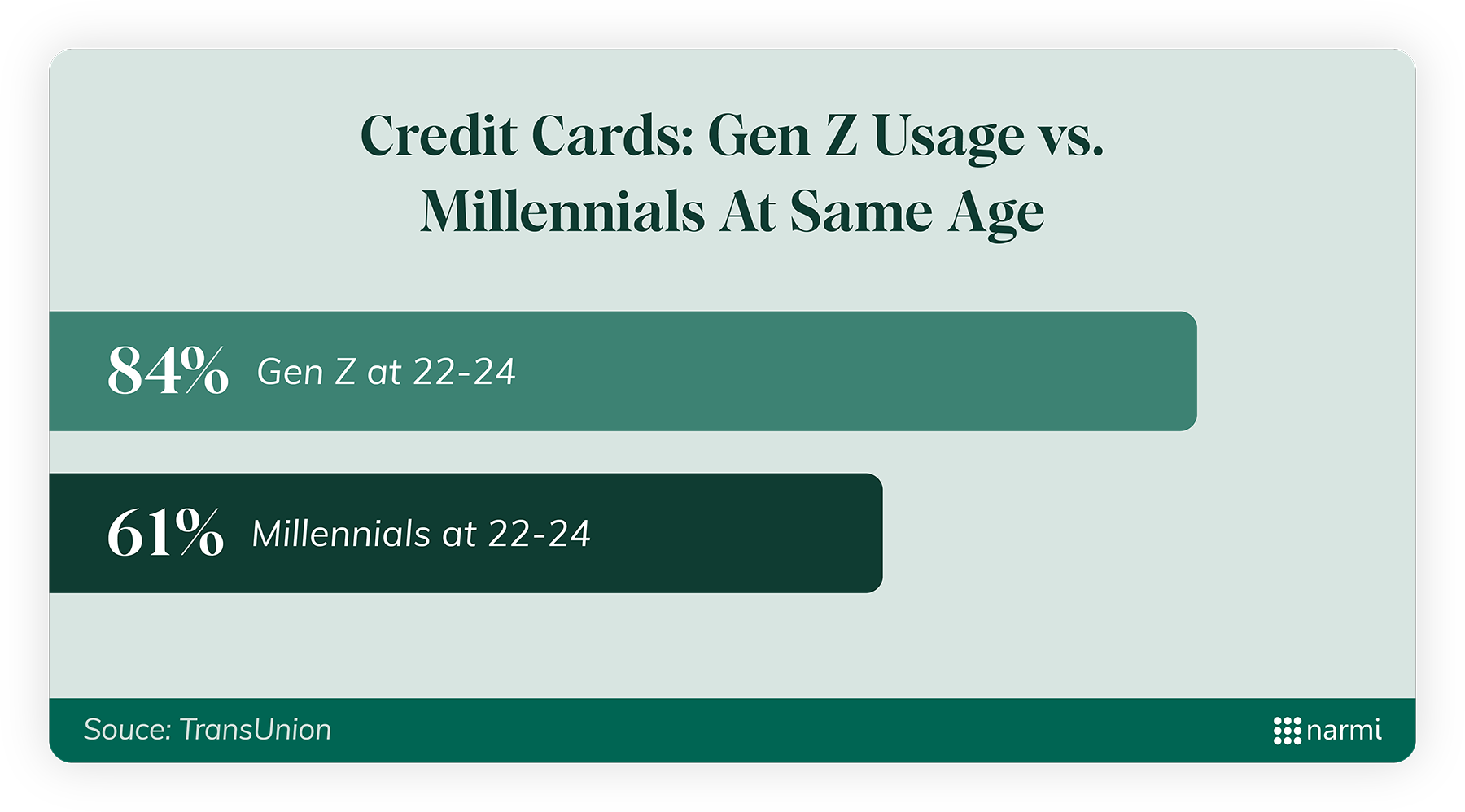

One of the clearest signals comes from generational credit patterns. A TransUnion study comparing Gen Z to Millennials at the same age (22–24) found:

Auto lending remains one of the most resilient consumer credit categories, but also one of the most volatile:

For banks and credit unions, this environment both creates a strong opportunity to cater to prime borrowers, who show healthy demand, and underscores the need for a large, diversified pipeline of loan applicants.

It’s widely understood that lending technology is a step behind its counterpart on the deposit side, which is among the reasons why dissatisfaction with a financial institution’s loan portfolio is generally attributed to a dearth of deposits.

But are banks doing the most they can to convert these deposits into attractive loan offerings? If we’re to shift the paradigm of seeing FI throughput from a “deposit gathering” problem to more of a “deposit optimization” problem, what considerations follow?

Digital is the lowest-hanging fruit: Corporate Insight found that among auto borrowers, 67% say a strong digital application matters; 40% consider it “very important” or “extremely important.”

Auto lending performance, like all other forms of lending, is increasingly tied to digital discoverability and execution. With younger borrowers not only using credit earlier, but making channel preferences like personalization and digital cohesion a part of their decision tree, financial institutions must shift their view on lending performance to not only account for providing the capital for these loans, but growing these pipelines through the high-intent relationships they’re already cultivating.

One of the most persistent misunderstandings in banking is the idea that weak loan portfolios are first and foremost a deposit problem.

Cornerstone Advisors’ 2025 report found that many FI CEOs still view deposit gathering as the core challenge: 52% list deposit gathering as a top concern, but only 19% of bank executives and 27% of credit union executives list a weak economy/loan demand as a top concern.

Additional data points to a more balanced view: institutions must both successfully gather deposits and convert them into well-designed, well-timed credit relationships by creating demand, not just tweaking their underwriting rules.

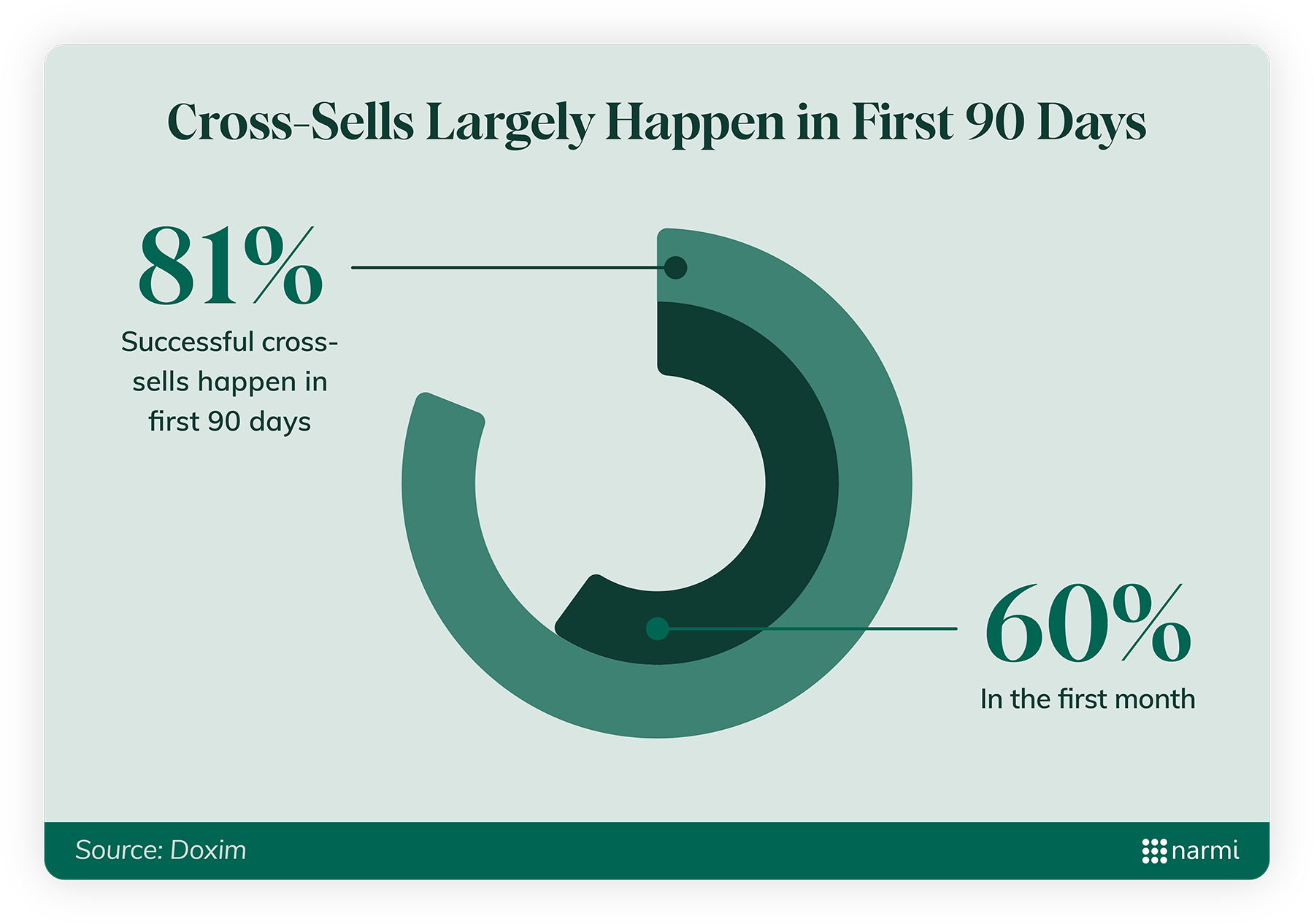

This conversion moment is sharper than many realize.

This is the moment when lending can most effectively “attach” to a new depositor. And it’s the moment when digital friction can do the most damage.

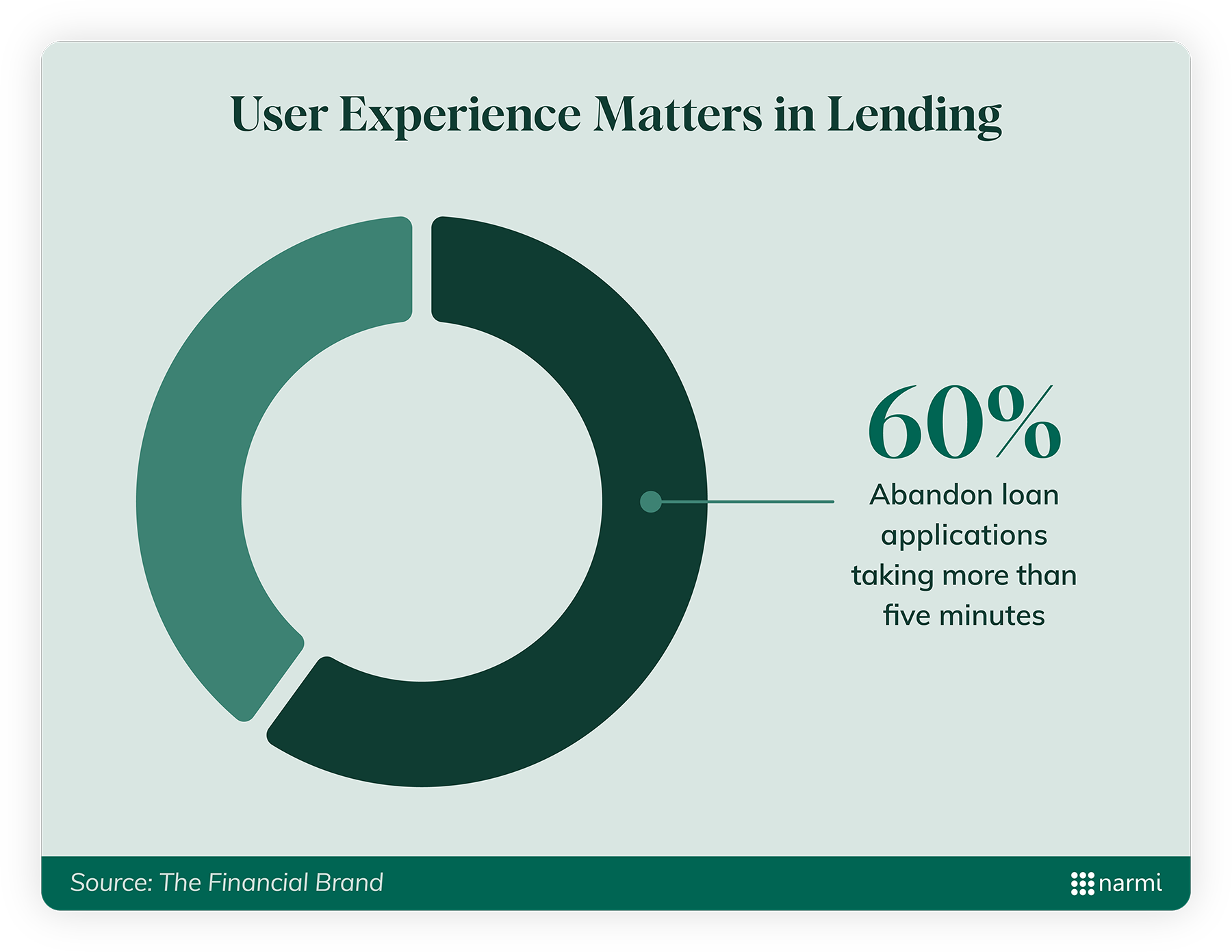

The lending experience has become a competitive filter. Borrowers, especially younger ones, will not wrestle their way through a 20-minute application, no matter how attractive the rate:

Clean, unified digital design isn’t window dressing. It is the single strongest determinant of whether a borrower completes an application or disappears, and to acknowledge this is to recognize that latent within your digital banking experience is the makings of a true demand generation channel for lending.

For more information on leading digital solutions to increase demand in lending, check out Narmi Lend.