For modern banks and credit unions, keeping up with feature-rich challenger banks and megabanks is a struggle. This is true even for the most forward-thinking financial institutions. Thankfully, there is a way for regional banks and community credit unions to stay competitive and provide the digital banking experiences people have come to expect. That path forward is Open Banking.

If you haven’t already, we recommend reading our post covering the basics of Open Banking and what it means for U.S.-based financial institutions.

But, knowing how financial institutions can actually benefit and extend the value of their digital offerings through Open Banking has been difficult to understand. That’s where Open Platform Banking comes in.

Here’s everything you need to know about API-powered Open Banking platforms, and the key benefits for financial institutions:

Open Platform Banking is an operating model that allows financial institutions to partner with innovative fintech vendors for all their digital, mobile, and online banking services.

Through a digital banking platform, financial institutions gain access to modern digital banking features and robust cloud-native infrastructure without having to invest in expensive development processes and commit to lengthy timelines. And as the name suggests, a banking platform lays the technological foundation for banks and credit unions to build upon to meet the specific needs of their customers and members.

It’s here that the benefits of Open Banking are most visible. Open platforms give developers the ability to create custom features and functionality that blend seamlessly with the existing user experience of the platform. In turn, banks and credit unions can choose from a marketplace of fintech solutions and bundle a wide range of services into one cohesive experience.

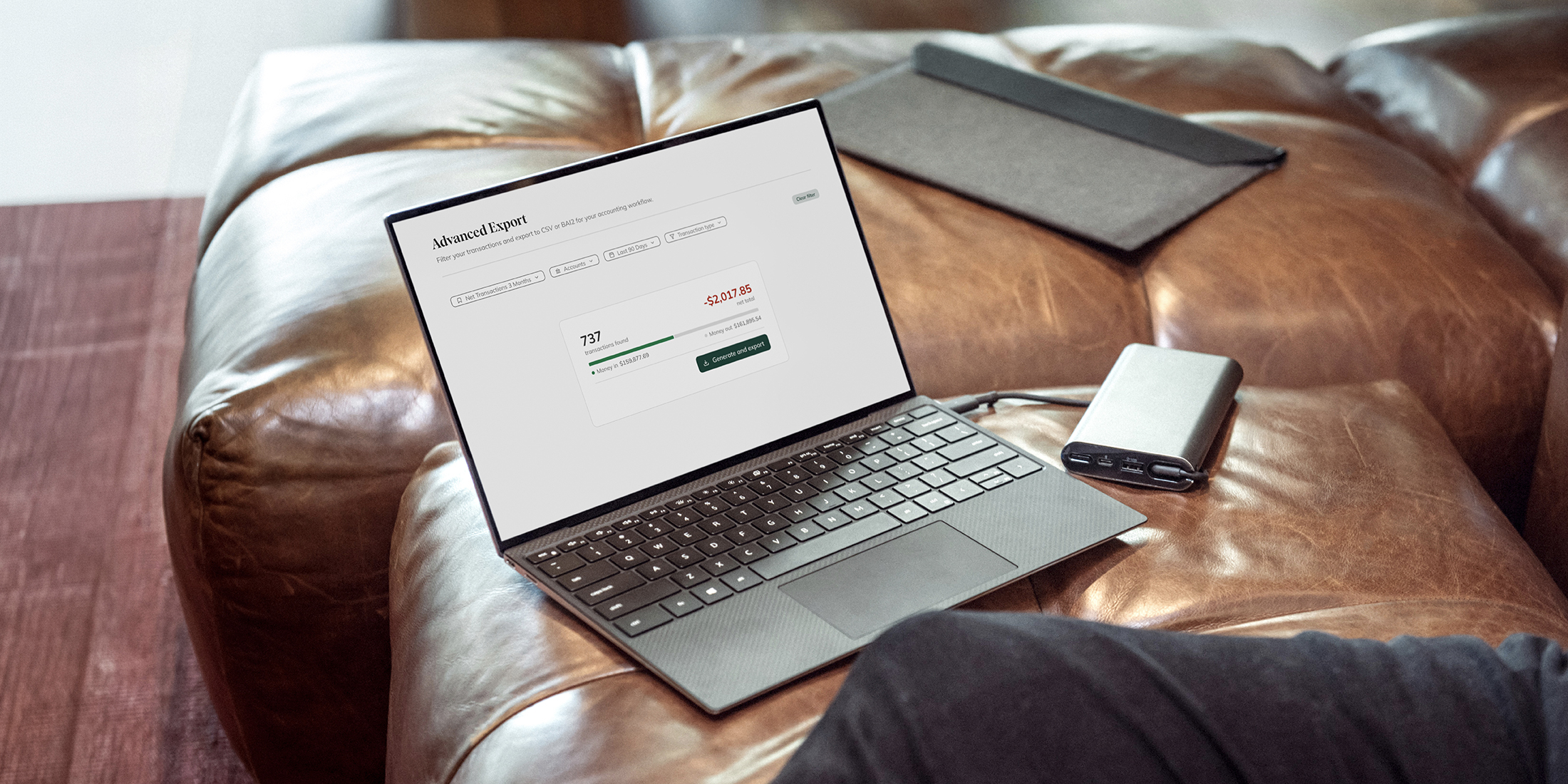

Platform-based banking is made possible through Open APIs and Open Frameworks. At both the core banking level and within the digital platform, APIs serve as translators between data sets and create a universal environment for developers. So instead of having to write code for each specific integration – using naming conventions specific to that system – a developer can write to one commonly understood language.

As a digital banking platform designed to integrate, Narmi creates an Integration Layer that allows our platform to speak with all core banking systems. And by maintaining our own API Integration Layer, we can ensure that we’re always taking the most modern approach to those core integrations.

.jpeg)

This API layer not only erases the idiosyncrasies of connecting across separate core banking systems, it also creates a robust Open Framework that gives developers a blank canvas. Our Open Framework – the Narmi Application Framework (NAF) – allows developers to build features that integrate directly into the application without having to learn the nuances of each core banking system.

This way, user experience and financial literacy principles can play a greater role in the product development process. And when banking platforms take an open approach to development by offering an Open API – as is the case with Narmi – third-party fintechs and financial institutions are able to work together to build custom functionality and features that integrate flawlessly and match the look and feel of the digital applications.

Platform-based banking offers some very attractive benefits for credit unions and banks, as well as their end-users. Here’s what we consider to be the main benefits of choosing a Platform Banking operating model:

The flexibility of an Open Banking platform is attractive to financial institutions looking to meet the specific needs of their customers and members. This is especially true of regional banks and credit unions who bank more niche individuals and businesses.

Being able to choose from a marketplace of platform add-ons and build custom functionality is a powerful way for these institutions to differentiate themselves from their competitors and evolve with their communities.

Fintechs are able to innovate much faster than traditional banks and credit unions for a few reasons, chief among them being their attractiveness to top engineering and product development talent.

With better talent, agile project management, unified product vision, and a healthy level of investment from venture capital firms, fintechs have been able to outpace traditional financial institutions.

Fintechs also have the ability to rigorously test the functionality and usability of their products – absorbing the risks associated with new technology and innovation. By the time a feature is ready to go live across the platform, financial institutions should be able to trust that it’ll work flawlessly for their end-users.

We regularly hear frustrations from digital transformation teams at financial institutions who are fed up with the limitations of their core-provided digital banking services. Rather than being at the whim of a sluggish development timeline, an Open Banking platform makes it possible for banks and credit unions to independently build custom functionality and have much more control over the development process.

Building and maintaining a proprietary digital banking platform would require a very large investment on the part of a financial institution. With a vendor-managed platform, credit unions and banks can keep their developer costs and IT infrastructure overhead low while accessing the most modern digital banking features and the dependability of a robust cloud-native infrastructure. It’s a win-win!

Perhaps the most compelling benefit for a platform-based approach is that it puts powerful digital banking tools in the hands of financial institutions, complementing the strengths they’ve already cultivated. Banks and credit unions can leverage their brand recognition, earned community trust, and expertise in compliance and regulatory best-practices, and choose a digital platform provider that’s right for them and their customers.

Without a wealth of in-house developer resources, it can be difficult for banks and credit unions to envision how they’ll be able to differentiate. Given that many digital banking features once seen as “disruptive” are now becoming expected features by consumers, it’s time financial institutions shift mindsets away from product-focused development in favor of a customer-centric approach.

.jpeg)

Being able to build a tailored online and mobile experience for the personalized needs of your customers and members is what’s going to help you move the needle for immediate growth, and continue to have a competitive edge down the road.

With a digital banking platform that can support flexible growth and personalization, it’s possible to take the feedback from your customers and members and turn it into features that plug directly into the digital platform. The end result is a digital platform that’s able to stay competitive with megabanks and challenger banks, and open up new opportunities for cross-selling bundled services – all with one beautiful and consistent user experience.