Experiences, not features, are what define an amazing banking product. And yet, financial institutions wanting to be seen as innovative strive to differentiate based on the digital banking features they offer.

The main problem is that many of the features that were once considered disruptive – like mobile check deposit, bill pay, and budgeting tools that help people understand their spending and save more – are now becoming baseline expectations for digital banking users. On top of that, many of the larger established banks have been able to learn from the success of challenger banks and develop comparable features and functionality.

For community credit unions and regional banks to keep up with the feature-rich competition and quickly develop the experiences & functionality users need, the path forward is API-powered Open Banking.

The concept of Open Banking, at the most basic level, refers to the ability of financial institutions to securely share the financial data of their users with external third-party developers.

In the U.K. and E.U. countries, Open Banking is further defined by the PSD2 regulations. Passed as an effort to level the playing field for small banks and develop a set of secure standards for sharing financial data, these regulations have led to a rapid rise in fintechs that bundle API-enabled features and services.

But while some were able to take advantage of the new opportunities, other financial institutions in the U.K. and Europe were ill-prepared for the shift – struggling to meet deadlines for adopting Open Banking standards and dragging their heels on integrations.

Here in the U.S., financial institutions free of any looming deadlines and industry-wide mandates have been able to learn from their E.U. counterparts and make incremental shifts in the banking industry towards more openness.

While slow to adopt, the recent sea-changes in consumer banking needs brought on by the COVID-19 pandemic have further highlighted the urgency for more Open Banking partnerships that unlock new growth possibilities. For banks and credit unions reliant on core banking service providers, this means having open access to user data and an API-powered banking platform that can scale and adapt to the needs of their users.

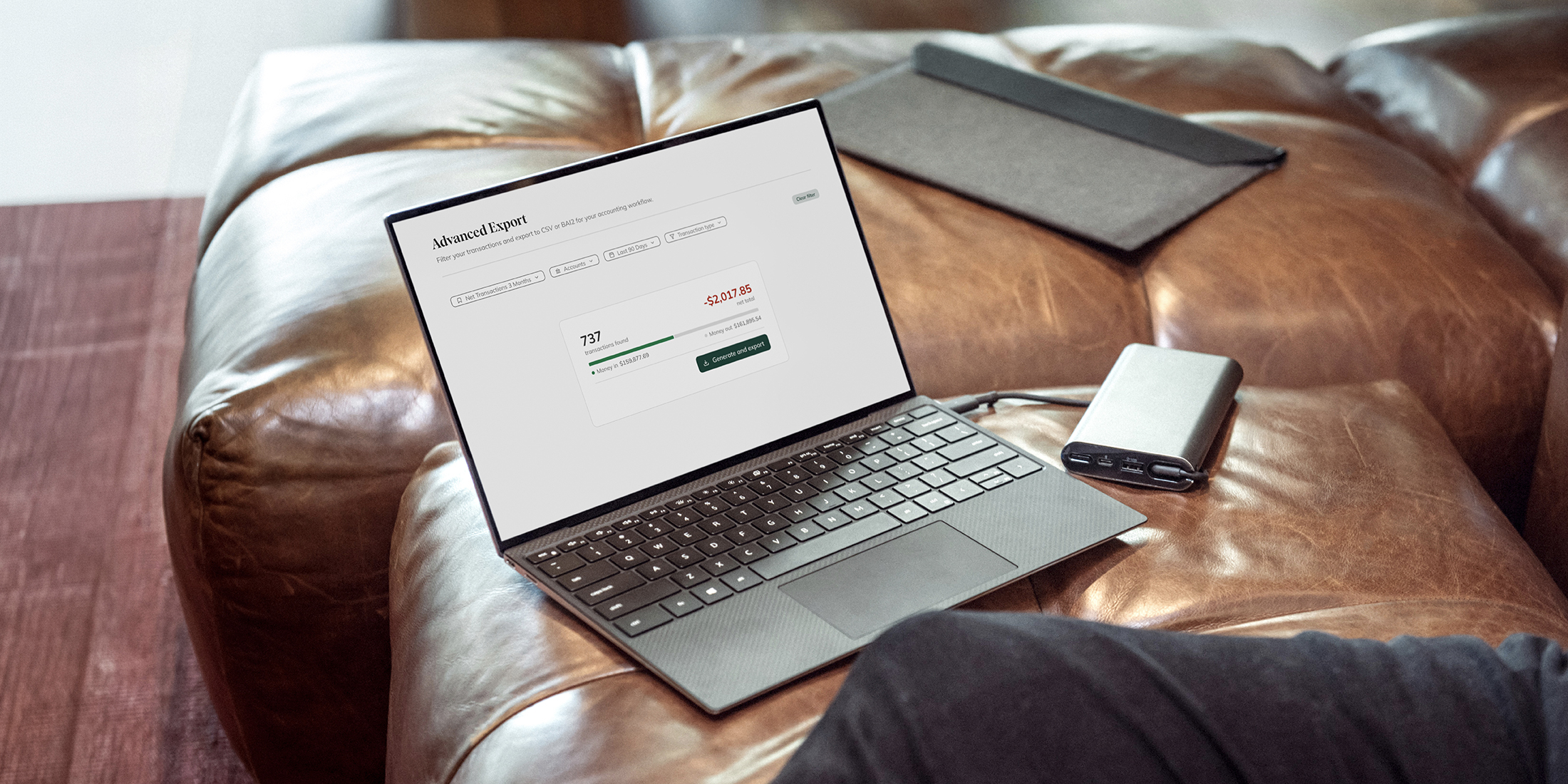

APIs are the technology that enables Open Banking and creates a standard way for developers to build applications that interface with user’s banking data.

Giving people the ability to choose what can be done with that data via APIs is an enticing opportunity for fintechs and forward-thinking financial institutions. By treating members and customers as co-owners of their financial data, credit unions and banks play the role of the stable and trusted financial partner. People can then seek out the apps and services that help them best manage their finances and choose the digital banking features that are right for them.

And while some may see this as giving away the keys to the castle of valuable data, others can look to the success of services like Alexa and Google Assistant which have been able to grow their market share and integrate into more aspects of daily life by opening up API access to voice controls. Within the U.S. payments and financial services sector, APIs allow vendors to bridge technology gaps and give users more control over their data. By bundling open payment services with other API-enabled data sets, ambitious startups are able to create unique solutions to everyday challenges.

Any time financial or personal data is shared, there’s a degree of risk that comes with it. As U.S.-based financial institutions have been observing the progress of Open Banking overseas, close attention has been paid to potential weak links and new opportunities for bad actors as new data pathways are exposed.

However, the reality is that having a unified standard for sharing and authorizing access to sensitive data – a standard that can be insulated from risk with multiple levels of encryption and elastic cloud-native infrastructure – is far more secure and scalable than alternative forms of data sharing, like screen-scrapers that ask users to share their login credentials.

In the absence of clear governance on how the U.S. banking industry handles data security across the board, the burden of discovering the best-practices for protecting privacy and staying in compliance falls on the shoulders of financial institutions. This, too though, presents an opportunity for local and more regional banks and credit unions. Rather than change occurring from the top down, financial institutions with strong ties to a community’s trust can educate their users and take their time to find the right fintech partners and banking services vendors they feel will be the best caretakers for their user’s needs and data privacy.

Maintaining the trust of users is essential for the longevity and growth of financial institutions as they start to envision a post-pandemic future. As more investment is made in the digital transformation of banking, it’s equally important to thoughtfully invest in the experience users have within an online or mobile banking product.

With demand for more controls over data on the rise from digital consumers, it’s crucial for banks and credit unions to shift mindsets around data. Once users are considered co-owners of their banking data, financial institutions can leverage APIs to develop personalized experiences and access a marketplace of fintech solutions that seamlessly integrate into digital banking platforms and prioritize the needs of the user.