For businesses managing payroll, vendor payments, and multi-account cash positions, bank reconciliation isn’t a back-office afterthought. It’s a daily necessity. And for the accounting and ERP systems those businesses rely on, there’s one format that has defined how bank data flows into the ledger for nearly four decades: BAI2.

Until now, delivering BAI2 to commercial clients has been a painful, expensive process for community financial institutions. Narmi’s native BAI2 and CSV Export changes that, giving FIs a real-time, on-demand export capability built directly into the digital banking platform, no core file transmission required.

BAI2 has been the cash management reporting standard in North American banking since 1987. Its staying power comes from something simple but powerful: every code means the same thing, no matter which bank issues it. A code 165 is an ACH credit received at Grasshopper Bank, at JPMorgan, and at every other institution in between. That consistency is what allows businesses with multiple banking relationships to pull data from all of them into a single ERP or treasury management system and have it reconcile correctly.

The demand is only growing. Commercial and mid-market businesses running treasury management systems and multi-entity accounting workflows treat BAI2 as a baseline expectation, not a premium feature. And while SMB ERP adoption is already widespread (80% of small and midsize businesses with annual revenue under $50 million now use ERP systems, a market growing at 10.7% annually), even smaller businesses with sophisticated accounting needs are starting to ask for it. When a community FI can't deliver, these businesses don't necessarily leave outright, but they start routing their more complex financial activity to larger institutions that can. Over time, those workarounds quietly erode the FI's case for being the primary banking relationship.

For community FIs that have supported BAI2 historically, the process has worked like this: the FI contracts with their core provider to generate a daily BAI2 file, which the core transmits to the digital banking provider, which then makes it available to the end user. On paper, that’s functional. In practice, it has three serious problems.

First, the data is stale. A file generated and transmitted at 2:00 AM reflects the world as it was at 2:00 AM. Any backdating, error corrections, or same-day adjustments that happen after transmission are invisible until the next day’s file, or never. Second, the FI usually pays a fee to the core for the daily process of generating and supplying the files, a cost that adds up and is difficult to justify for FIs with only a handful of commercial clients who need it.

Narmi's native BAI2 export eliminates the need for the core file transmission entirely. When a business is enabled for BAI2, Narmi uses transaction data it has retrieved from the core via API and delivers an export accurate to that instant. Backdating corrections and error adjustments are reflected immediately because Narmi is reading current data, not a snapshot from a file that arrived hours or days ago.

There is also an advantage in how BAI2 code translation is handled. Traditionally, FIs had to work with their core to set up and maintain the mapping of core transaction codes to BAI2 codes, paying a license fee for the privilege. With Narmi, setup is a one-time configuration: the FI sends Narmi a mapping file specifying how their core transaction codes correspond to BAI2 codes, and Narmi takes it from there. If the bank ever needs to update or refine those mappings, they can do so without opening a ticket with their core.

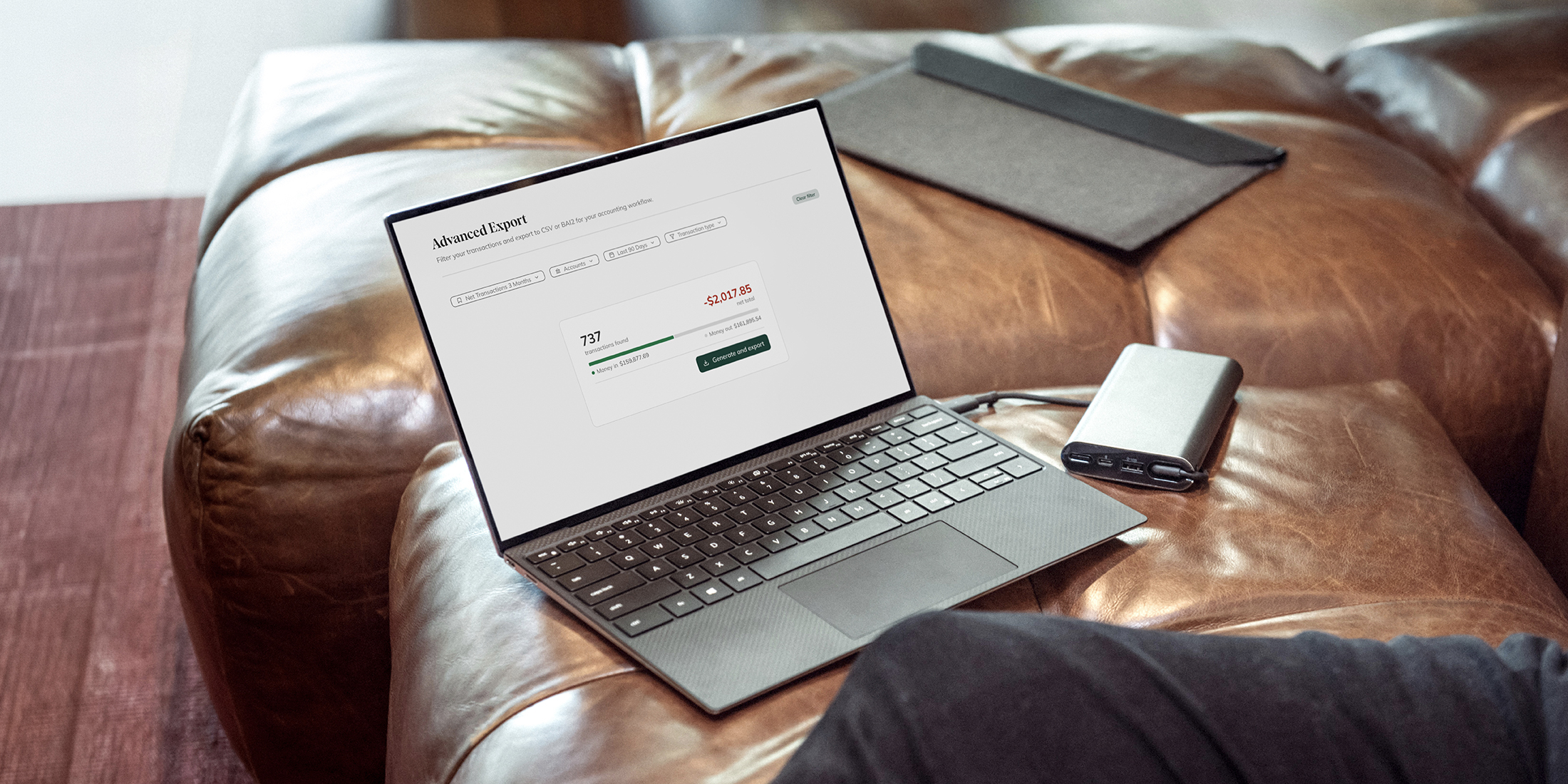

Business users access the feature through a new Reports tab in their digital banking experience. From there, the Advanced Export tool gives them several practical controls: they can pull transactions across multiple accounts in a single export, a capability most single-account transaction views don’t support. They can filter by date range, selecting a single day, the prior week, the current month, or a custom window. They can narrow results by specific BAI2 transaction codes, so a controller who only needs to verify outgoing wires doesn’t have to sort through unrelated activity. Before exporting, they see a summary of money-in versus money-out totals as a quick cash flow reference. And they can save frequently used filter configurations as named views, making weekly or monthly reporting runs repeatable with a single click.

Both BAI2 and CSV export formats are supported. CSV extends the feature’s reach to businesses that use accounting software outside the traditional treasury management ecosystem, broadening the value without adding complexity to the user interface.

With native BAI2 and CSV Export, community financial institutions can give their commercial clients the same on-demand, most current account data that businesses expect from the nation’s largest banks, while maintaining the personalized relationships and lower cost structure that define who community FIs are. For any FI looking to grow its commercial portfolio, this is the kind of capability that turns a transaction into a long-term banking relationship.