Delivering on your customers’ and members’ digital expectations has never been more critical, which is why more institutions are (or should be) taking a closer look at their real-time payments strategy. Demand for real-time payments has exploded in recent years - 70% of U.S. consumers and 90% of businesses say having access to faster payments is a vital satisfaction driver. However, many financial institutions have yet to deliver a true real-time payments solution to their customers and members, partly because the implementation costs have been too high or the ROI is unclear.

However, the recent launch of The Federal Reserve’s FedNow Service may be driving institutions of all sizes to re-evaluate their real-time payments approach. Designed as a low-cost, flexible payments rail, FedNow may drive significant real-time payment adoption in the U.S. Hundreds of financial institutions have already implemented FedNow, and many more indicate plans to adopt it, suggesting that a real-time payments adoption race could be on the horizon.

Investing in a new digital payments solution is a big decision that requires institutions to think closely about the needs of their customers. But while real-time payments might seem like a “nice to have” banking feature, it may be the linchpin for delivering value to individual and business customers in the fight to capture and maintain core deposits.

Here are three critical use cases for the FedNow Service and how they can deliver impact to your customers and members:

Let’s start with the obvious use case: real-time payments allow customers and members to make a payment within seconds. There are quite literally infinite use cases for this functionality, but ones that stand out as essential banking transactions might be:

The intrinsic value of a real-time payment is that both sender and receiver get the peace of mind of knowing the money was transferred instantly. For business customers that thrive on efficiency, instantly paying vendors and suppliers or even their employees immediately upon receipt of a product or service allows them to manage their cash better and free up that working capital to be put elsewhere. Most importantly, FedNow’s instant payment framework operates 24/7, 365 days a year - meaning users can make these payments at any time, not just during regular banking hours. This is significant because many other options currently available to customers and members such as ACH payments and wire transfers are considered “faster” payments but are not instant and can be costly to initiate.

Real-time payments users tend to focus on the payments portion, but instant money transfers are an equally attractive feature of services like FedNow. Individuals can transfer funds between their accounts at different financial institutions or fund new accounts or mobile wallets. Again, the tangible value of this functionality is offering peace of mind, whether a customer or members is looking to avoid a late or overdraft fee or feel more in control of their money. Instant money transfers might also be particularly important for businesses in the wake of the collapse of Silicon Valley Bank when many banking customers scrambled to access and transfer their funds to avoid payroll issues or delinquency on payments.

There’s arguably no better sell for real-time payments than giving users the ability to receive money instantly rather than waiting days for a transaction to clear and such as requesting a payment from a friend on Venmo, eliminating those uncomfortable situations like chasing someone down for money owed. Instant payment requests can help expedite traditionally slow business transactions like an insurance payout or tax refund. For business users, an added benefit of payment requests through FedNow is the ability to include an e-invoice that details all the information they need for their back-office records when the payment is remitted. This feature is especially helpful for smaller businesses that may not have as robust tracking systems or currently rely heavily on more manual processes.

As mentioned previously, institutions of all sizes may be implementing or planning to implement FedNow or another real-time payments service in the coming months, increasing the risk of your institution falling behind in the adoption curve. At the same time, FedNow implementation isn’t a simple flip of the switch. As a result, it is better to start thinking about your strategy sooner rather than later. To launch FedNow and ultimately drive user adoption, institutions will want to consider how it integrates into their existing digital banking experience, the potential impact on their existing transaction processing or fraud prevention framework, and a multi-channel communication strategy.

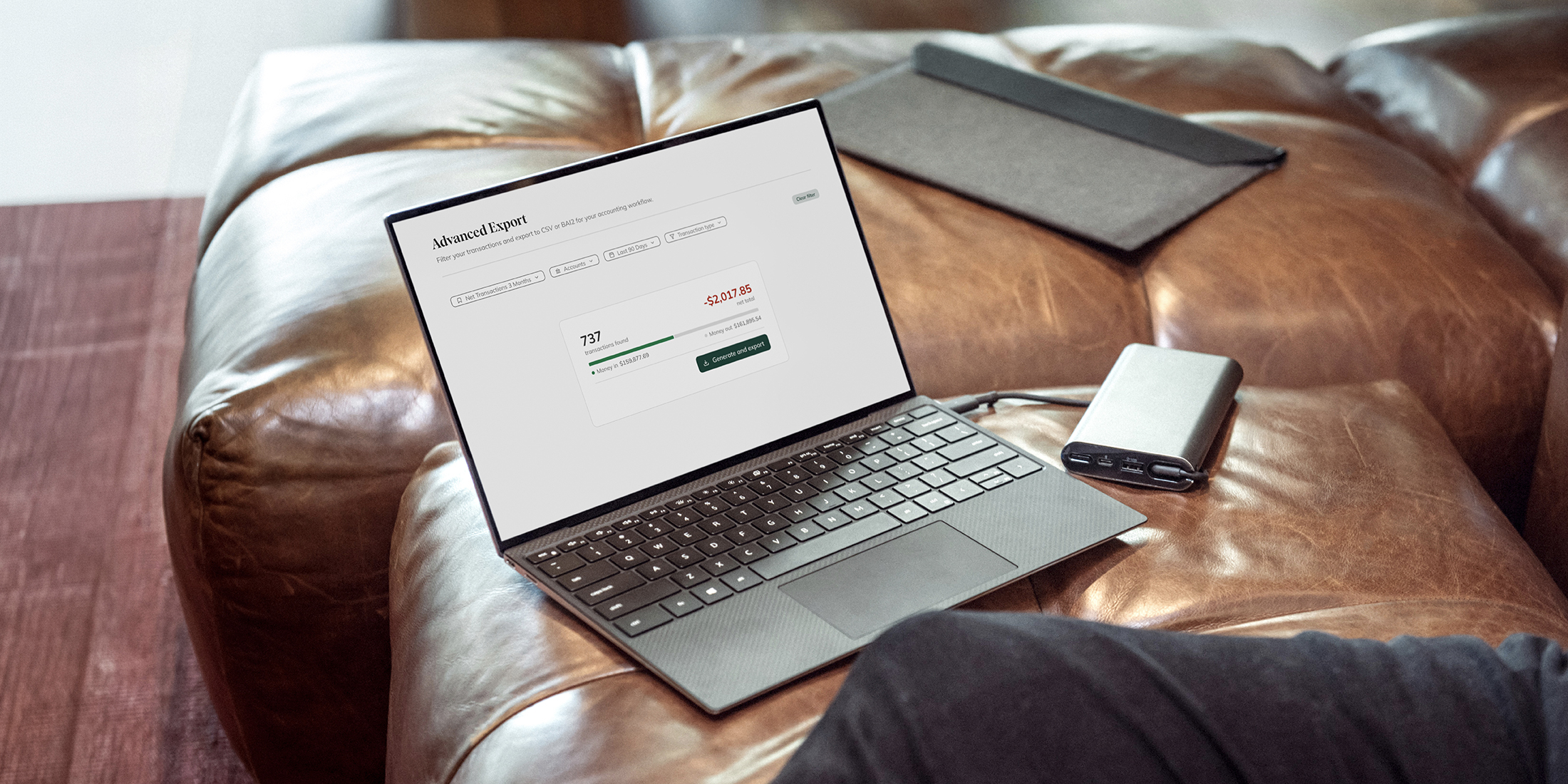

As a full service provider of FedNow, Narmi is integrating FedNow natively into our digital banking experience through a phased rollout. We are also here to answer questions and have helped numerous institutions create a preparedness and launch timeline.