0. Introduction

1. Put the user experience first

2. Throw existing processes “out the window” and automate where possible

3. Open accounts digitally, quickly, and safely

4. Seamlessly transition between account opening and mobile/web banking

5. Serve the customer digitally

6. Master the interaction with the primary brand

7. Understand the economics

8. Correctly leverage your core banking system

9. Conclusion

With the rise of challenger banks (N26, Chime), deposit-taking fintechs (SoFI, Acorns) and deposit-taking technology firms (Google, T-Mobile), the ~11,000 financial institutions in the United States have been forced to refine their business models and prepare for a different competitive landscape compared to the one they’ve faced over to the last 20 years.

This refinement is a very healthy exercise and the best financial institutions are ahead of the curve, preempting changes in the sector rather than reacting to them, incorporating new technologies, and constantly looking for ways to offer customers new solutions to interact with them and their products.

One idea that has become popular with financial institution executives is the concept of starting an independently branded, or co-branded, digital bank or digital brand. The thesis revolves around the notion that starting fresh with a new brand potentially solves several problems facing financial institutions today as they try to move into a “digital-first” way of doing business.

Narmi is part of a large number of these conversations and has outlined what the playbook looks like for implementing a digital-only brand. While this insight piece is geared towards financial institutions considering implementing a digital brand, financial institutions can also apply this playbook to their core brand and therefore their entire organization.

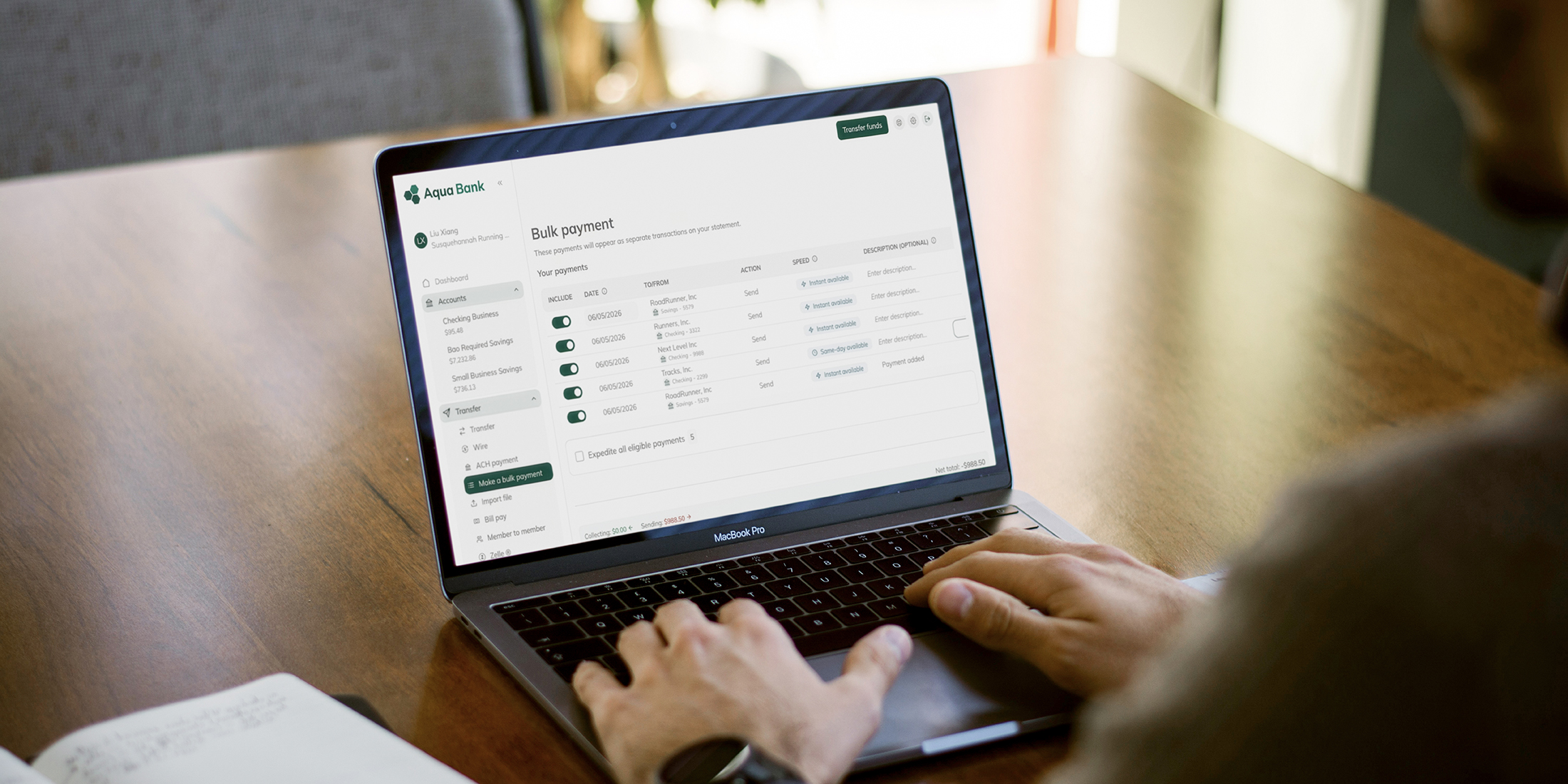

Financial institutions must put experience first when developing and releasing new functionality. The most successful digital brands will offer strong functionality and deliver it via a superior user experience. This may be a deviation away from existing practices, which often force financial institutions to yield to legacy processes or serve existing customers the way they have been served for years.

Consumers and businesses expect digital transactions to be seamless, intuitive and immediate. The appetite for a clunky banking experience is small, and financial institutions can build loyalty in the form of increased deposits and additional accounts by offering a better user experience. Experience should therefore be a driver of process, not a byproduct.

Another way to think about user experience is across the various functions that touch a digital brand. The goal with any digital-first offering is to offer a comprehensive and seamless experience from start to finish across the entire user experience. The core areas to think about are...