In the ever-evolving landscape of finance, deposit growth stands as a pivotal marker of success for financial institutions. However, shifting consumer behavior and increasingly volatile market conditions are proving traditional methods of capturing deposit growth to be insufficient. This has led to a burgeoning interest among financial institutions in leveraging technology to effectively target small businesses (“SMBs”) - an largely underserved banking segment - for deposit growth.

There are several reasons why small businesses represent a significant source of potential deposit growth for financial institutions. For one, small businesses are a major part of the banking population and a cornerstone of economic activity; McKinsey estimates that the U.S. is home to over 30 million small businesses that represent around $150 billion in annual revenue or about 17% of the entire banking industry.

SMBs rely on their core deposit partners for a variety of business functions, from cash flow and treasury management, to payments acceptance, and payroll and accounting. Because of this, small business deposit accounts tend to be funded at higher levels and more actively managed than consumer deposit accounts, providing financial institutions with a more reliable foundation for balance sheet stability.

Lastly, small businesses are less tied to any single institution and are likely to have multiple deposit relationships. In the wake of the Silicon Valley Bank crisis, SMBs have become more discerning about where they keep their money and one study found that two-thirds of SMBs are more likely to look for new primary banking relationships. That’s a lot of deposit activity that will be up for grabs.

Nurturing relationships with small businesses is important not only for deposit growth, but also for building trust and loyalty with this massive segment of the banking population with complex financial needs.

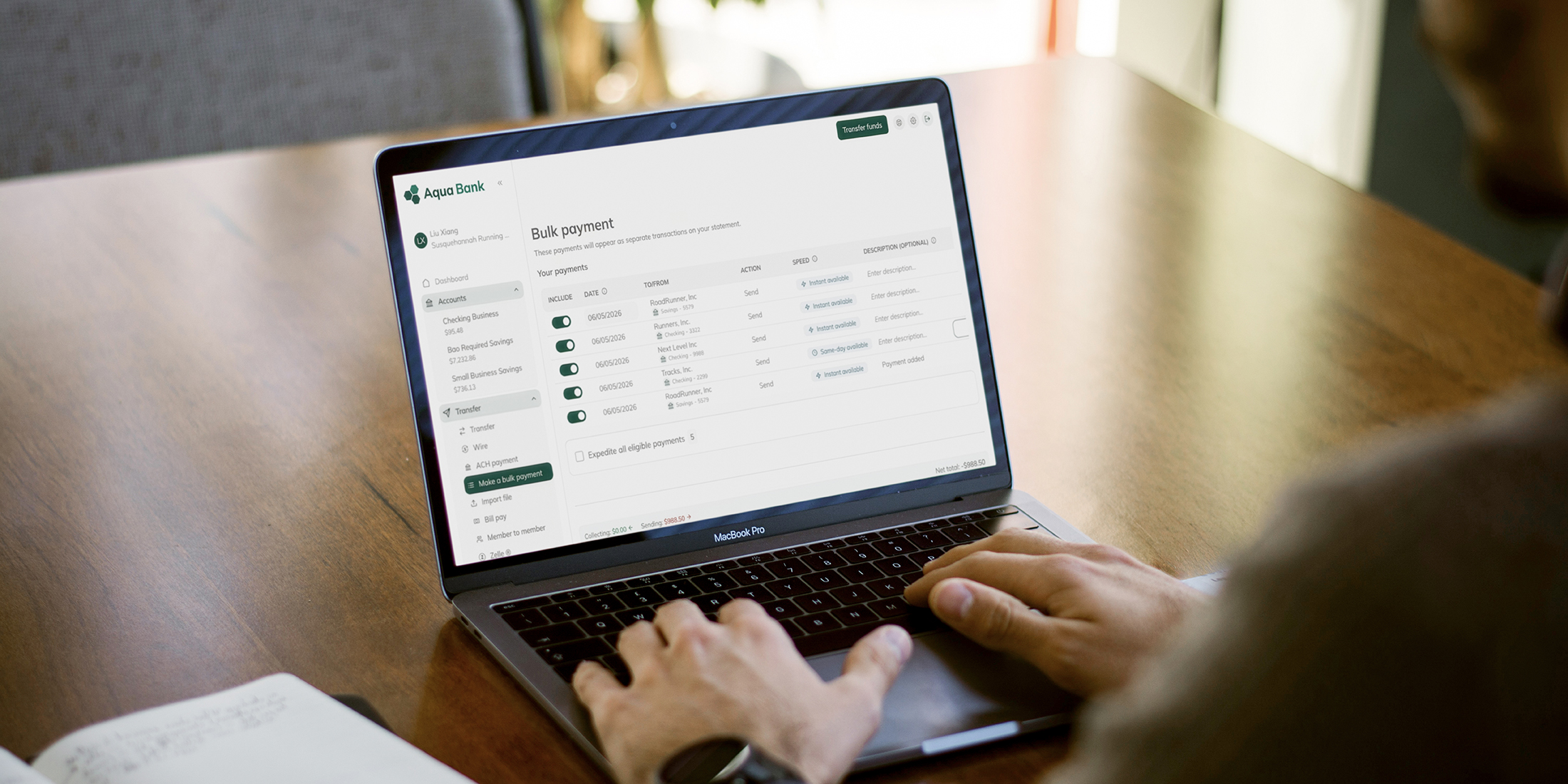

To capture small business deposits, financial institutions need to deliver banking solutions that meet the needs of small business owners. Consider three key deposit-based use cases of a business banking account, and what the average business owner would likely need to make their job (and life) easier:

But beyond individual features and functionality, SMBs want a banking partner that is easy to do business with, and that means a digital-first experience. 60% of small business owners said online banking capabilities were a key factor in deciding where to bank. This digital expectation starts at the account opening process and extends through business owners’ ongoing interactions with their banking partner. Therefore, to meet SMBs’ digital expectations, financial institutions must be willing to embrace a digital-first mindset, offering tailored digital banking products and analyzing customer data to identify and serve their unique needs and preferences.

Of course, building a world-class business banking experience to capture deposit growth isn’t exactly simple or cost-effective for most financial institutions. As small businesses demand more comprehensive financial management tools, more robust self-service features, and more personalized bank offerings, financial institutions will need to find a way to address those needs without blowing up their technology budget. This is where fintech partnerships can create a mutually beneficial opportunity for financial institutions and small businesses alike.

Collaboration with fintechs can help institutions bridge the gap between traditional banking services and technology innovation. Instead of a “buy or build” approach to new business banking products and features, partnerships with fintechs allow institutions to integrate the solutions their customers need into their existing offering. Imagine being able to integrate the bookkeeping tools and payment providers that business owners use every day, without having to expend significant resources or wait for length development cycles. Adopting this level of technology integration through an open banking platform - allows financial institutions to deliver the tools and services their business banking customers need at scale and create a “stickier” overall digital experience.

Ultimately, capturing SMB deposit growth and achieving bank primacy will require institutions to be more than just a venue for business owners to deposit or withdraw money. Business owners want and need a digital banking partner that is going to improve their operational efficiency and support their long-term business growth.

By leveraging technology to make it easier for business owners to fund their deposit accounts, and giving them tools to automate manual processes related to managing cash flow, payments, and day-to-day business operations, financial institutions can build deeper relationships that demonstrate they’re more than just another banking provider.

In conclusion, the pursuit of small business deposit growth represents a compelling opportunity for financial institutions. By understanding the needs of small business owners, embracing a digital-first mindset, and partnering with fintechs, institutions can unlock sustainable growth avenues and achieve primacy.

As evidenced by the evolving landscape of finance, technology stands as a catalyst for innovation and progress, underscoring its indispensable role in achieving this shared objective. Embracing this paradigm shift, financial institutions can navigate the complexities of the modern market landscape and emerge as leaders in driving deposit growth through small businesses.